Equity valuations are having an Icarus moment. For more than

a decade, the cost of capital fell. The post GFC

dis-inflation or the lack of inflation meant central banks

kept bringing down rates, even to negative territories in

certain markets. Central banks also pumped significant

liquidity into markets, especially in the wake of the

pandemic, which depressed yields even more (Chart 1).

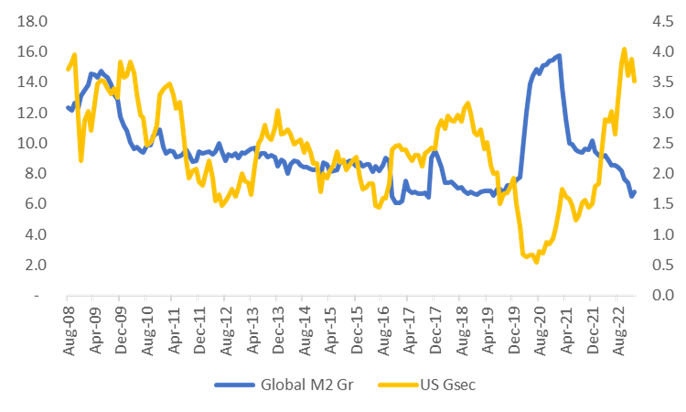

Chart 1: Global M2 YoY growth and US Treasury yields (as a

proxy for global bond yields)

Source: SBIFM Research

Source: SBIFM Research

Cheap and abundant money became the ultimate stimulant for

risky assets. Markets disregarded all concerns on inflation

or yields. QE became the new normal as the beast of

inflation had been tamed, or so it was believed.

The heady rise in inflation in the last 12-18 months is

breaking the back of ever-rising p/e’s. Monetary policy

moves to counter rising inflation have spiked bond yields,

and thus, as a corollary the cost of equity. The Orcus of

inflation is merrily slashing away the excesses of the last

decade.

The average P/E of ~BSE200 companies (curated for outliers)

has corrected from ~38x in the post pandemic rally to ~27.5x

at end of March 2023. The correction, some would argue

(especially value investors), has been long overdue.

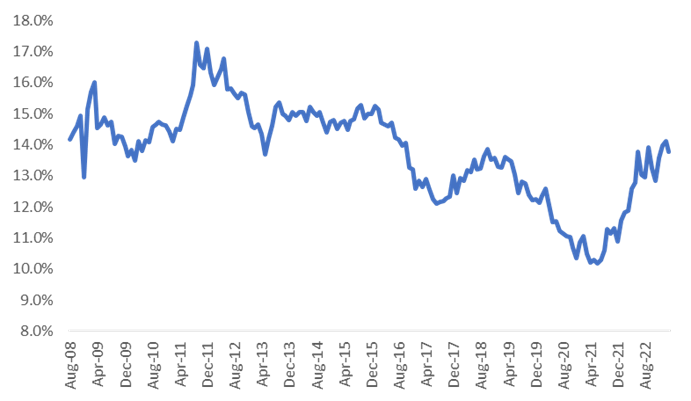

Observed cost of equity (using the Damodaran formula and

data) for a 1 beta firm in India fell from the 16-17% to the

10-11% mark over 2010/11 to 2020/21. And is now at the 14%

mark.

Chart 2: Cost of Equity for a 1X beta firm in India

Source: SBIFM Research. Calculation is done using the

principals laid out by Prof. A. Damodaran

Source: SBIFM Research. Calculation is done using the

principals laid out by Prof. A. Damodaran

The BSE200 constituent’s curation has been done for sharp

outliers (those having ‘absurd P/Es’ such as 500-1000x, loss

making periods, etc)

If falling yields were a driver of cheaper equity capital,

the inverse should hold true as well. Yields have risen on

higher rates and a reversal of QE to QT, consequently the

cost of equity has risen. The chart below shows the degree

to which the two are directionally correlated.

Chart 3: Calculated cost of equity v/s Indian 10-year

G-Sec yield

Source: SBIFM Research

Source: SBIFM Research

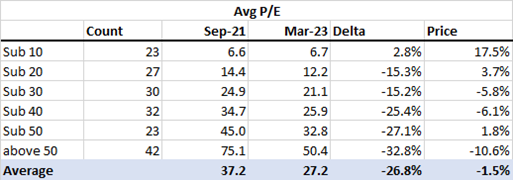

The chart below depicts the move in the avg p/e of ~BSE200

constituents (curated). Each dot represents the Avg p/e

compared to the cost of equity (at 1 beta). The red dot

represents March ‘23, The dot yellow is the peak of Sep ‘21.

It is worth noting how much it has corrected in just a year

(Purple to Red)

Chart 4: X Axis - Cost of Equity, Y Axis - Avg P/E of

~BSE200 constituents

Source: SBIFM Research

Source: SBIFM Research

The average P/E of the curated BSE 200 constituents has

corrected by 12.9% compared to the p/e 2 years back (Mar ‘23

v/s Mar ‘21). The most intriguing change has been the FMCG

pack, which has seen the average p/e remaining flat. The

Industrial Pack has seen a 5.5% increase, which is not

surprising given the increased investor interest in the

potential for a new industrial cycle.

Table 1: Delta in P/E at the end of Mar 23 sector wise

compared to Mar 21.

|

Avg P/E delta Mar 23 v/s Mar 21

|

| Commodities |

-4.3% |

| Consumer Discretionary |

-17.9% |

| Diversified |

-45.0% |

| Energy |

-10.7% |

| Fast Moving Consumer Goods |

1.2% |

| Financial Services |

-27.0% |

| Healthcare |

-12.5% |

| Industrials |

5.5% |

| Information Technology |

-10.6% |

| Services |

-42.4% |

| Telecommunication |

-25.4% |

| Utilities |

18.7% |

| Average |

-12.9% |

Source: SBIFM Research

The delta in p/e changes is uniformly the highest for those

which rose the most. The tables below depict the delta in

avg p/e in various buckets. In table 2, there were 42 stocks

part of the BSE200 which had a p/e above 50 in Sep 21, those

stocks had an average p/e of 75x which has corrected by

~33%. In contrast in Mar of 2013 (table 3) there was only 1

stock which had a p/e above 50x.

To keep things in perspective, in the 50+ p/e bucket, for

the stock price to remain flat, earnings would have had to

grow 49% over this period. The average stock in this 50 p/e+

bucket returned ~-11%.

Table 2: Delta in P/E at the end of Feb 23 by various

buckets from the peak of Sep 21.

Source: SBIFM Research. Arithmetic averages for price

performance and P/E

Source: SBIFM Research. Arithmetic averages for price

performance and P/E

For the universe the average stock return was -1.5% and the

p/e correction was 26.8%, essentially all earnings growth

was eaten away by the p/e compression. The chart below

decomposes the 1 year return of the Nifty from earnings and

from valuations. As can been seen, recent earnings growth

has been eaten away by the fall in valuations. Price, one

pays matters. Excessive valuations will eat into earnings

growth.

Chart 5: Nifty 1 year return decomposed by earnings factor

and valuation factor

Source: SBIFM Research

Source: SBIFM Research

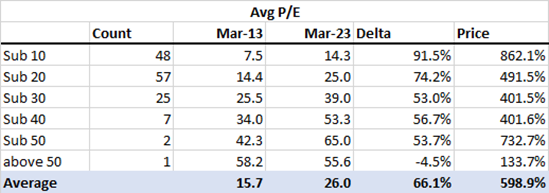

The ten-year data (Table 3) is in some sense not surprising.

The highest average return has been from the lowest p/e

bucket of companies. These would have seen a dual impact of

rising earnings as well as rising p/e’s.

Table 3: Delta in P/E at the end of Mar 23 by various

buckets from the peak of Mar 13

Source: SBIFM Research. Arithmetic averages for price

performance and P/E

Source: SBIFM Research. Arithmetic averages for price

performance and P/E

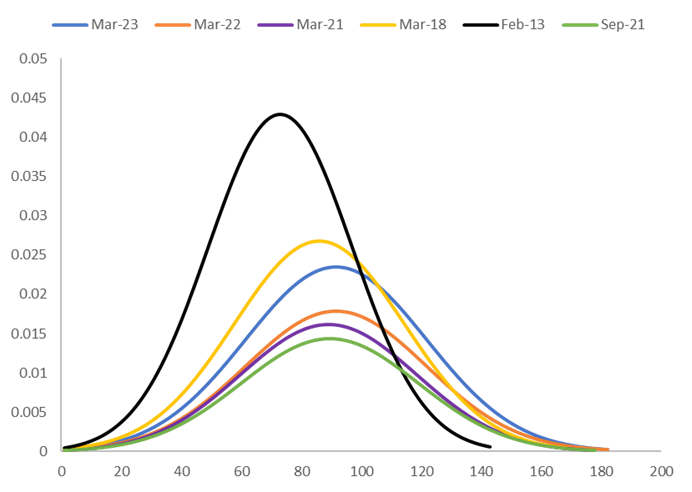

So what lies ahead? The normalized bell curve for

p/e’s (chart 6) shows a narrowing of the std deviations and

a fall in the mean p/e (from 37.1x in Sep 21 to 27.5x in Mar

23). Still, from a 10-year perspective, average p/e’s are up

2/3rd’s. The average multiple is at 26x for a cost of equity

not so dis-similar, 13.8% in Mar 23 compared to 14.6% in Mar

13.

Chart 6: Normalized bell-curve of p/e’s across time

periods.

Source: SBIFM Research

Source: SBIFM Research

This probably implies that if earnings don’t accelerate fast

enough, we run the risk of mediocre equity returns at best

or a price correction. Earnings have been supportive so far,

but the future could see turbulence with growth expected to

slow. The wings of easy money over the last decade exalted

many market participants and securities. There have been

meaningful corrections, but pockets of exuberance and

valuation excesses remain.

We may, of course, be blessed by central banks once again

with a pivot as the rate rise cycle pauses but it is far

more likely that rates will remain at a higher levels than

move back to historic lows. This means that cost of capital

will remain elevated shifting the conversation back to

earnings growth. This transition is unlikely to be smooth.

Odds are that it’ll likely be a stock pickers market and

that much harder to generate returns you were used to.

This presentation is for information purposes only and is

not an offer to sell or a solicitation to buy any mutual

fund units/securities. The views expressed herein are based

on the basis of internal data, publicly available

information & other sources believed to be reliable. Any

calculations made are approximations meant as guidelines

only, which need to be confirmed before relying on them.

These views alone are not sufficient and should not be used

for the development or implementation of an investment

strategy. It should not be construed as investment advice to

any party. All opinions and estimates included here

constitute our view as of this date and are subject to

change without notice. Neither SBI Funds Management Limited,

SBI Mutual Fund nor any person connected with it, accepts

any liability arising from the use of this information. The

recipient of this material should rely on their

investigations and take their own professional advice.

Appendix:

-

GFC =

Great Financial Crisis of 2008 which resulted in

collapse of Lehman Brothers and severely affected

several financial firms across the globe

-

QT =

Quantitative Tightening – When the central bank makes

money dearer/expensive

-

QE =

Quantitative Easing – When the central bank makes

money easier/cheaper

-

PE =

Price to Earnings Ratio – A relative measure of value

of a company

-

Orcus* -

Latin god of underworld who punishes broken

promises/oaths, used here as an analogy representing

Inflation acting like Orcus and punishing people who

committed valuation excesses in the last cycle

-

Damodaran =

Prof Aswath Damodaran of New York Stern School of

Business. His work can be accessed here:

https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/wacc.html

)

12e76bb30b4a4c748257d262c6e2e347)

)

)