The Indian money market serves as the primary channel for

short-term funding across banks, public financial

institutions, non banking financial companies (NBFCs),

Housing Finance Companies (HFCs) and large corporates.

Certificates of Deposit (CDs), largely issued by banks,

and Commercial Papers (CPs), issued by corporates and

financial entities, form the backbone of this ecosystem.

On the demand side, mutual funds constitute the dominant

investor base in these instruments.

Recent developments suggest that the money market has

entered a phase characterized by elevated CD issuance

(Exhibit 1), structurally wider spreads, low CP issuances

by corporates, alongside an ever-prevalent feature of low

secondary liquidity

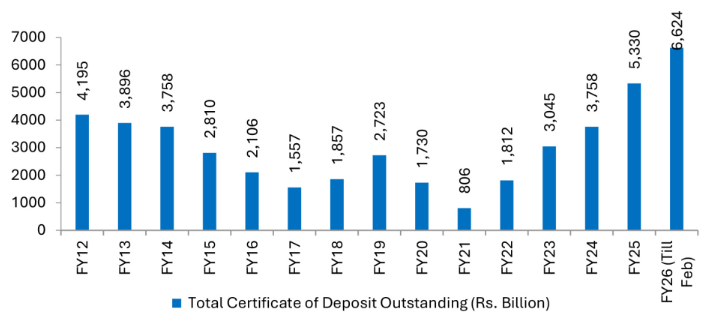

Exhibit 1:

Certificate of Deposits (CD) by Scheduled Commercial

Banks issuances rise

Source :

RBI, SBIFM Research

Source :

RBI, SBIFM Research

However, unlike earlier episodes of stress, particularly

the post-IL&FS period of 2018-19, current conditions do

not appear to stem from credit deterioration. Instead,

they reflect a complex interaction between structural

investment preferences by retail investors, and regulatory

requirement of Liquidity Coverage Ratio (LCR) by banks,

seasonal Asset under management (AUM) patterns for mutual

funds, and portfolio construction preferences within the

mutual fund industry.

Structural liquidity tightening and expansion of CD

issuances

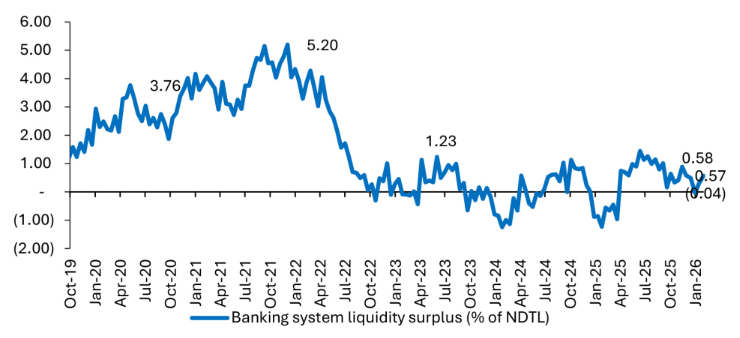

From mid-2023 onwards, banking system liquidity began

normalizing after a prolonged period of surplus conditions

(Exhibit 2). Banks, that had earlier relied comfortably on

deposit growth, increasingly faced challenges in

mobilizing incremental deposits at competitive rates. At

the same time, credit offtake began to show signs of

revival. Since 2022, barring a brief period of Oct-2024 to

Oct 2025, bank credit had been healthy and has outpaced

the deposit growth (Exhibit 3). Even now, bank credit has

recovered sharply from the May’2025 lows of 9% to 14.5% by

Jan 2026, with most banks revising their credit growth

guidance for FY27 upward. This combination-deposit

mobilization pressures alongside steady credit

demand-pushed banks toward greater reliance on wholesale

funding through CDs (Exhibit 4).

Exhibit 2:

Source : RBI, SBIFM Research; NB:

Banking system liquidity refuse to net LAF

surplus

Source : RBI, SBIFM Research; NB:

Banking system liquidity refuse to net LAF

surplus

Exhibit 3:

Bank credit growth has been outpacing deposit

growth…

Source : RBI, SBIFM Research

Source : RBI, SBIFM Research

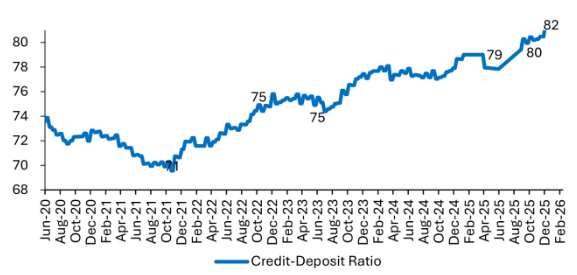

Exhibit 4:

...thereby pushing up the system system-wide

credit-deposit ratio to elevated levels

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Outstanding CD issued by scheduled commercial banks rose

significantly, expanding from approximately Rs. 3 trillion

at the start of 2023 to ~Rs. 6 trillion by end Jan 2026.

Jan and Feb 2026 witnessed particularly strong issuance

activity. This shift reflected banks’ emphasis on resource

mobilization, especially in the context of quarter-end

balance sheet considerations and improved loan growth

momentum.

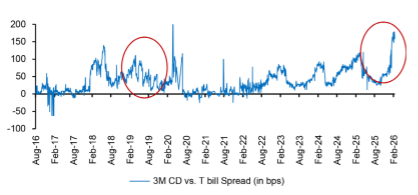

Alongside higher issuance volumes, spreads on CDs relative

to 3-month Treasury Bills widened meaningfully (Exhibit

5). After an initial softening following policy rate cuts

during 1H 2025, spreads began rising steadily from

July’2025 onward, moving from roughly 30–40 basis points

to 75-80bps by end 2025 and touched even 175bps by

Feb’2026 over relevant T-bill. The current spread levels

are even higher than those observed during the liquidity

dislocation of 2018–19. However, unlike that period, the

present widening does not reflect concerns over asset

quality or counterparty risk; instead, it mirrors

structural supply-demand imbalances and the funding needs

of banks operating under tighter deposit conditions.

Exhibit 5:

3-month CD spreads have widened to ~175bps against

T-bill by end January 2026

Source : Bloomberg, SBIFM

Research

Source : Bloomberg, SBIFM

Research

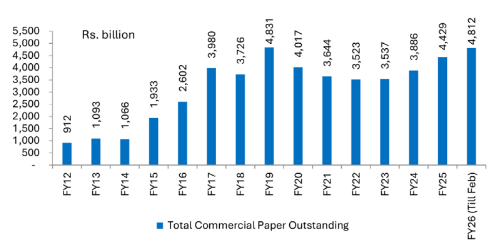

Exhibit 6:

Total CP outstanding is nearly INR 2 trillion lower

than CDs outstanding

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

What explains high CD issuances but low CP issuances by

corporates ?

While CD supply surged (i.e. the short-term funding needs

of banks surged), the Commercial Paper (CP) market is

experiencing a noticeable moderation (Exhibit 6).

Corporates that had previously accessed short-term

markets, reduced or halted CP issuance. CP spreads are

relatively more compressed. This is because anecdotal

evidence suggests that bank working capital lines linked

to external benchmark lending rates (often T-bills plus

some spread) are cheaper than likely CP yields. Clearly,

the latter is more cost-effective. To sum, corporate

borrowing from money market is low due to more attractive

rates being offered by banks.

The CP market consequently became concentrated in issuance

by NBFCs, housing finance companies, and select public

financial institutions. As corporate CP volumes

diminished, the breadth of tradable names has narrowed

significantly, further reducing market depth, especially

beyond very short tenor.

While the supply is rising, demand appetite for money

market instruments is weak

On the demand side, mutual funds constitute the dominant

investor base in the money market instruments.

While CD issuances are on the rise, the fund flows in the

relevant mutual fund schemes, which can subscribe to money

market papers, is limited. To give some backdrop, the

Indian mutual fund framework imposes clear limits on

duration and credit risk through SEBI’s category

classification system. Each debt category has prescribed

Macaulay duration limits and weighted average credit score

requirements. Funds cannot freely migrate to riskier

profiles without regulatory and documentation changes.

In practice, this structure enforces discipline but

reduces flexibility during volatile periods. Liquid funds,

for example, cannot invest beyond 91 days, while overnight

funds are restricted to one-day instruments such as TREPS.

Furthermore, equity and hybrid funds often maintain cash

balances for margin requirements related to futures

positions, and these balances cannot be freely deployed

into longer-dated CP or CD instruments.

As a result, headline liquidity metrics-such as large

volumes in the collateralized TREPS market—overstate the

amount of AUM available for CD and CP deployment (Exhibit

7). Only a subset of debt funds has both the mandate and

the risk appetite to meaningfully invest beyond overnight

instruments.

Exhibit 7:

Average daily volumes in overnight segment

Source : RBI, SBIFM Research

Source : RBI, SBIFM Research

Taxation changes and AUM reallocation in debt mutual

funds

Changes in debt mutual fund taxation announced in Union

budget 2023 and made effective April 2023 significantly

altered the attractiveness of debt mutual funds for retail

investors by aligning taxation with marginal income tax

rates (Exhibit 8). Further in July 2024 budget, the

indexation benefits enjoyed by debt mutual funds, held for

over two years, were removed. This reduced the post-tax

return advantage of any debt funds relative to bank fixed

deposits.

Exhibit 8:

Taxation changes in debt mutual funds in India

announced in Union budget 2023

Source Budget documents, SBIFM

Research

Source Budget documents, SBIFM

Research

Consequently, incremental flows into duration-oriented

debt categories have been subdued. Instead, AUM growth has

concentrated in overnight funds, which serve primarily as

corporate cash management vehicles. Liquid fund and money

market AUM has increased in line with nominal growth,

while mid to longer-duration categories have experienced

either stagnation or modest outflows

Also, incremental flows since April 2023 in pure debt

funds is now predominantly institutional and corporate,

with retail participation skewed toward hybrid and equity

categories. This shift increases managed AUM volatility,

as institutional capital is inherently more tactical and

liquidity sensitive.

Substitution from mutual fund liquid schemes to bank bulk

deposits

As banks’ struggle for both CASA (current and savings

account) and sticky fixed deposit, deposit mobilization

challenges has led banks to deploy both CD issuances and

bulk deposits as a tool to raise funds. While Mutual funds

subscribe to Bank CDs, they are a competing product to

banks’ bulk deposits. Banks’ bulk deposits do not have

daily MTM adjustments and offer competing returns to

mutual funds, thereby turning out to be a more preferred

investment avenue for some corporates in recent times.

Thus, apart from taxation, the increased bulk deposits by

banks are also driving reduced inflow into mutual fund

schemes.

Secondary market Illiquidity and market concentration

Despite large outstanding volumes of CDs and CPs, actual

secondary market liquidity remains limited (Exhibit 9).

Trading activity is concentrated in very short residual

maturities, often within 30 days, and primarily in

high-grade names. Insurance companies and provident funds

are largely absent from this segment, while banks

participate selectively, mainly for liquidity coverage

ratio (LCR) management and largely restricted to AAA

exposures within its residual maturity.

Exhibit 9:

Total Secondary Market Trade (reference period December

2025)

Source :CCIL, RBI, SBIFM

Research

Source :CCIL, RBI, SBIFM

Research

As a result, mutual funds frequently are the only

remaining secondary trading partners. However, given that

redemption patterns are often synchronized across fund

houses, selling pressure tends to emerge simultaneously

across participants, reducing effective bid-side depth.

This structural asymmetry constrains duration rebalancing

and encourages conservative, diversified portfolio

construction. Funds are compelled to avoid concentration

risk and illiquid exposures. The illiquidity in CP markets

is especially pronounced. Outside a small set of

high-quality issuers, exit opportunities are limited,

reinforcing a hold-to-maturity bias among investors.

Furthermore, limited secondary market depth forces

investors to demand additional spread compensation for

liquidity risk.

Seasonality and flow cycles in Mutual Funds

Seasonality also plays a central role in shaping money

market dynamics. Every March, (as also around other

quarter end months) corporates withdraw significant sums

from liquid and money market funds to manage their balance

sheet and meet tax and reporting obligations. Banks also

attract short-term deposits during this period. As much as

20–25% of liquid fund assets under management (AUM) may

temporarily exit the system.

These funds typically return in April, generating strong

reinvestment demand and causing short-term rates to

decline. This predictable cycle influences portfolio

construction. For instance, in January and February,

mutual funds tend to avoid buying three-month papers to

prevent amplifying exposure to post-March reinvestment

risk.

Hence, there could be a mismatch between the tenor of

paper issued and preferred, thereby also accentuating its

impact on spreads. This recurring seasonal pattern

amplifies short-term volatility in spreads and issuance

preferences, even when underlying liquidity conditions

remain broadly stable as was the case in this financial

year.

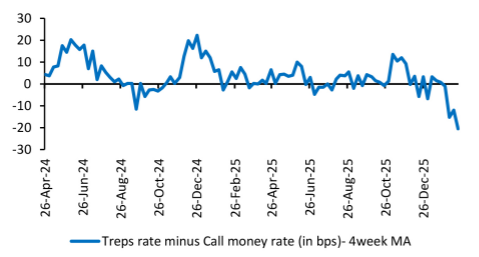

Comparative perspective and policy considerations

While CD rates are operating at a significant spread to

T-bills, there is a wide divergence in overnight rates.

There has been a good 25-50bps spread between TREPS and

interbank Call money rate- both key instruments in

overnight segments (Exhibit 10).

Exhibit 10:

TREPS signal excess Tri-party liquidity, yet money

markets remain unfunded

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

In developed markets such as the United States, money

market funds have direct access to central bank reverse

repo facilities, allowing overnight rates to align closely

with policy corridors. In India, non-bank entities lack

direct access to the Standing Deposit Facility (SDF), and

the bulk of overnight activity occurs in collateralized

segments such as TREPS. At times, this leads to meaningful

divergence between policy rates and collateralized market

rates. In current times, banks are borrowing in TREPS and

lending in RBI’s SDF platform- thereby sometimes earning

an arbitrage.

Broadening access to central bank liquidity facilities for

non-banks could potentially enhance rate transmission and

reduce volatility in collateralized segments. However,

such reforms would need to be weighed against monetary

policy transmission objectives and systemic risk

considerations.

Outlook on CD spreads in current times

There could be some moderation in CD spreads in April

after the March redemption cycle is over further the CD

supply could also moderate. Banks’s guidance suggests that

credit outlook stays healthy over the coming quarters. As

such, banks would be in continued needs of funds. However,

with current rise in CD rates, banks have seen a

flattening of yield curve in the borrowing space. This may

prompt them to gradually shift away from short-tenor CDs

towards longer tenor infrastructure and tier II bonds also

if their asset liability considerations permit.

Banks are generally restricted by regulation from issuing

regular long tenor non-convertible debentures (NCDs) and

can only issue infrastructure bonds if they have

infra-eligible assets. In FY26, there was a hiatus where

banks issued infrastructure bonds but lacked the

corresponding infra-eligible assets, which seems to be

resolved now, potentially allowing for increased supply.

There is a demand from provident funds and other long-term

investors for longer tenor papers. Hence, deploying such a

strategy could also help cooling CD spreads.

Conclusion

The current phase of India’s money market is characterized

not by credit fragility but by structural investment

pattern changes emerging from post-covid period and

frictional liquidity dynamics. The expansion of CD

issuance reflects banking system funding realities, while

the contraction of corporate CP issuance underscores the

competitive dominance of banks in an intermediated system.

On the other hand, mutual funds demand appetite has been

constrained by lack of flows in the desired schemes (both

due to taxation and better returns in competing bank

products), regulatory portfolio constraints, secondary

market illiquidity, and concentrated investor

participation. Thus, elevated CD spreads are best

understood as the equilibrium outcome of deposit

constraints, credit growth, and limited non-MF

participation.

Unless structural participation broadens or liquidity

mechanisms evolve, the Indian money market is likely to

continue exhibiting episodic mismatches between supply and

demand. These mismatches will remain a defining feature of

short-term rate behaviour, independent of underlying

credit fundamentals.

)

)

)

0bf21f855da944d2a0c843c4553297d8)