Section 3: Indian Macro

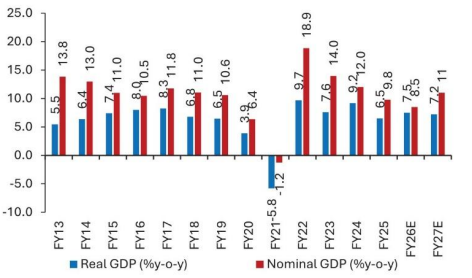

India’s 1H FY26 real GDP growth has averaged at 8% y-o-y

while the nominal GDP growth has been extremely soft at

8.8% y-o-y.

India’s economic activity had been soft in 1H FY26

Real GDP strength is at odds with modest growth in

several high-frequency indicators, including corporate

data. We maintain that Nominal GDP is the clearer

indicator of India’s economic pulse especially during

times when WPI is extremely low. Nominal growth,

presently, is much weaker than desired 11-12% (at the

very least).

High frequency indicators suggest a pick-up in activity

during November 2025

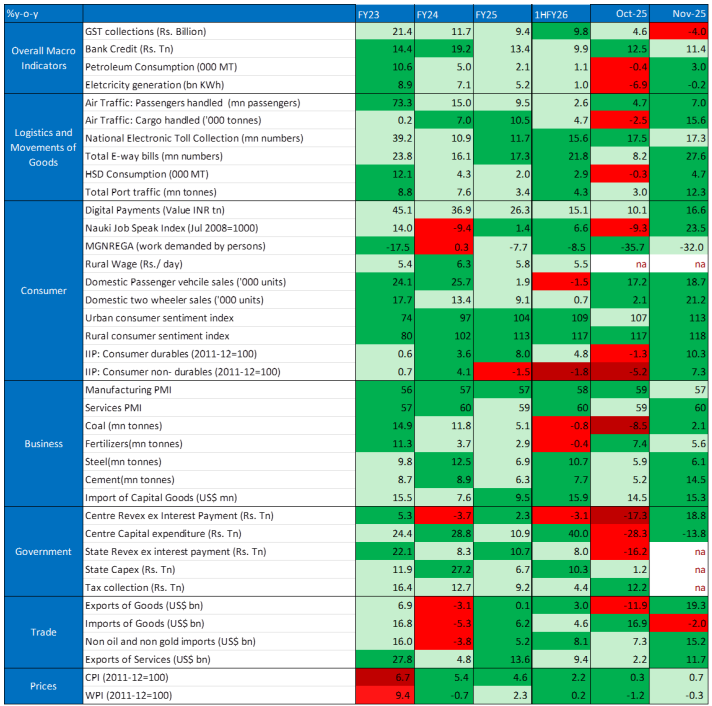

Looking beyond Q2, high-frequency indicators for

November show encouraging signs: a pickup in bank

credit, healthy services exports, freight activity

(likely aided by GST rate cuts and festive demand),

strong steel consumption, and resilient auto sales

especially for tractors, and passenger vehicles. Tax

collections have also improved in September and October

2025 (Exhibit 20).

Exhibit 20

High Frequency Indicators

Source: CMIE, RBI, SBIFM Research; NB: Dark

green denotes positive and higher than previous month,

light green positive but moderation, light red is

negative but improvement, red is negative and

deterioration

Source: CMIE, RBI, SBIFM Research; NB: Dark

green denotes positive and higher than previous month,

light green positive but moderation, light red is

negative but improvement, red is negative and

deterioration

Statistical anomalies could distort the GDP prints in

FY26 and FY27, but…

Purely for deflator reasons, FY26 real GDP could clock a

growth of 7.5% y-o-y while nominal could be low at 8.5%.

For FY27, we are getting incrementally positive on

India’s growth outlook. As the low inflation tailwinds

will be behind us, real GDP growth could appear to be

moderating to 7.2% but we expect nominal growth to

improve to ~11% in FY27 (Exhibit 21). It is important to

note that Ministry of Statistics is planning to release

a new GDP CPI and IIP series which will see a base

revision and some methodological changes which might

require us to revisit the statistical prints.

Exhibit 21

India’s Nominal and Real GDP outlook

Source CMIE, SBIFM Research

Source CMIE, SBIFM Research

…more importantly, directionally, we are positive on

growth in FY27 backed by policy thrust

One of the most important reasons for us to get positive

is the change in policy outlook. Both fiscal and

monetary policy were growth restrictive in 2024, with

monetary policy fixated on inflation and regulatory

tightening while fiscal policy focused on tax buoyancy

and consolidation. This has meaningfully reversed in

2025.

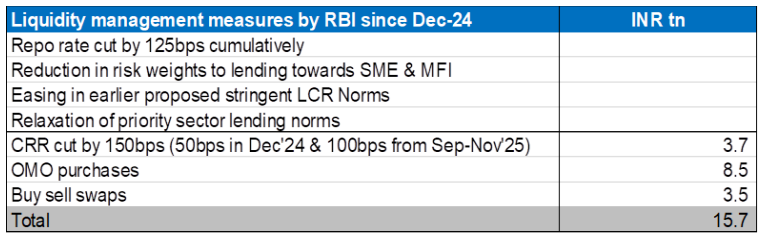

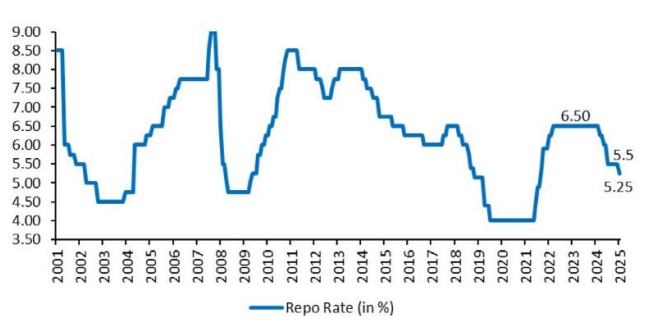

Monetary policy has shifted from risk aversion to growth

orientation in 2025

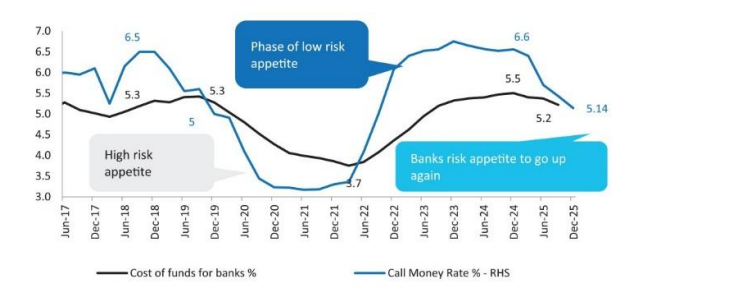

For banks, the regulatory stance has shifted from risk

aversion to growth orientation. Throughout 2025, there

has been tacit relaxation in credit-to-deposit ratio

norms, liquidity coverage ratio requirements, and

provisioning for unsecured loans. Repo rate has been

reduced by 125bps in 2025, and RBI has taken direct

liquidity infusion measures totaling to INR 15.7

trillion via OMO purchases, CRR reduction and FX swaps

and LCR relaxation since December 2024. Even as

liquidity had stayed lower than desired despite these

measures, the intent is quite clear- which is to keep

liquidity supportive.

Exhibit 22

Liquidity support by RBI since Dec’2024

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

From tax cuts to labour code: India’s reform surge in

2025

Further, the absence of a trade deal and the resurgence

of the current government’s popularity in multiple state

elections post-June 2025 appear to have catalyzed a

series of meaningful reforms during the year. The year

began with a reduction in personal income tax, followed

by GST rate rationalization, removal of quality control

orders in select sectors, implementation of the labour

code, 100% FDI in the insurance sector, permission for

private investment in the nuclear sector, and a revamp

of the employment guarantee scheme to enhance

efficiency. Overall, 2025 was a power-packed year for

reforms. It is also understood that several states have

become increasingly proactive in easing regulatory

bottlenecks to attract FDI, with Tamil Nadu setting a

notable example. While many of these reforms are

difficult to quantify in terms of their immediate growth

impact they undoubtedly contribute to a more

constructive outlook for India’s medium-term economic

story.

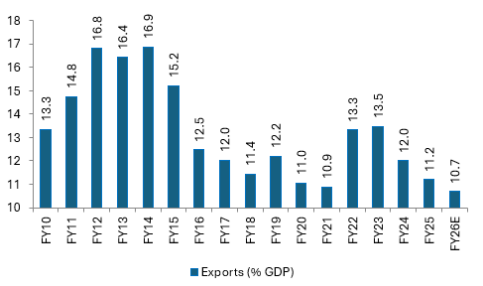

India’s Export Outlook: Waiting for Clarity Amid Trade

Deal Uncertainty

We remain hopeful that the India–US trade deal will

materialize in 2025, while India continues to sign free

trade agreements with other nations (Exhibit 23).

However, any export-related boost from such an agreement

is not factored into our current growth model, even

though it would likely improve sentiment around dollar

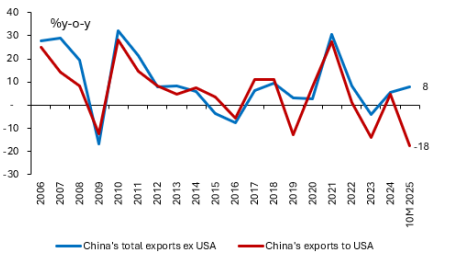

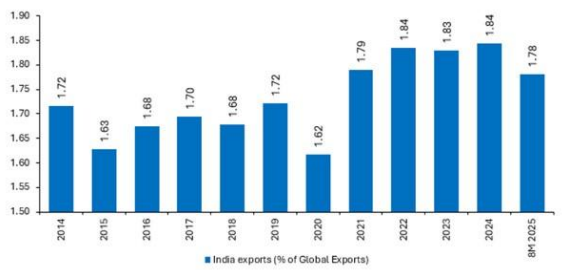

inflows and the rupee. At the same time, we are mindful

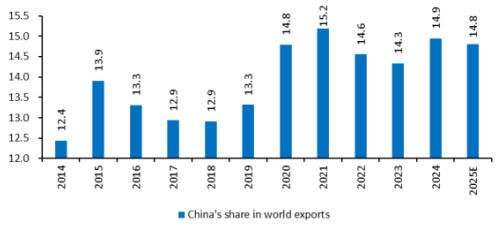

of rising competition from China, which continues to

capture a larger share of global trade, leaving India’s

market share stalled under 2% of GDP (Exhibit 24,25,26).

For now, we assume healthy services exports but a

subdued performance in goods exports. Interestingly,

November 2025 merchandise export data was surprisingly

strong, suggesting that India’s export dynamics have

remained resilient despite the 50% tariff imposed by the

US. Still, it would be prudent to wait for a few more

months before establishing a trend. It is too early to

conclude whether a trade deal would significantly boost

exports or, conversely, whether the absence of one would

lead to a meaningful decline. Given that US growth –

excluding AI-driven sectors – appears modest, and both

China and Europe lack significant momentum, we maintain

an unexciting outlook for India’s exports in 2026–27.

Exhibit 23

Bilateral Trade Agreements post COVID

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Exhibit 24

China continues to grab global trade share

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Exhibit 25

China’s exports ex of US surges

Exhibit 26

India’s global trade share has fallen in 2025

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Hence, growth will clearly by shaped by domestic forces.

Credit led growth recovery in cards

A true yardstick for success stories of government

reforms would be measured in the form of bank credit,

improvement in India’s manufacturing share to GDP,

formalization of labour force and increased FDI in

India. One of them has already started to improve.

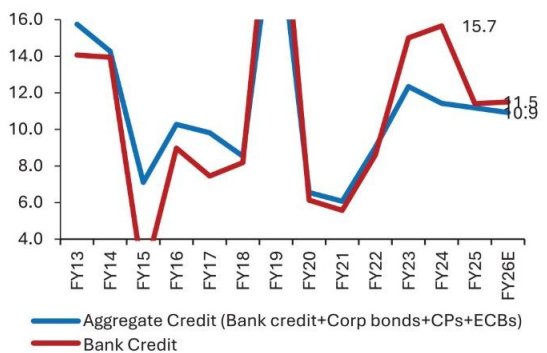

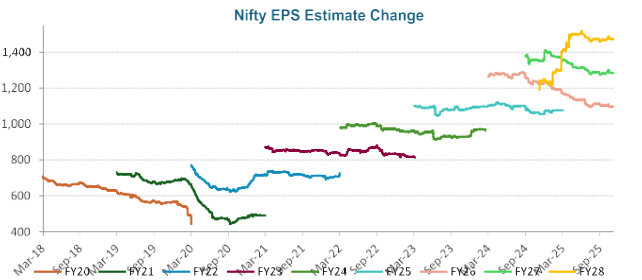

Bank credit which has improved from 9% in May 2025 to

11.5% by end November 2025 (Exhibit 27). We expect it to

further improve to 13-14% in FY27. Adding up the other

avenues of credit (NCDs, CPs and ECBs), aggregate credit

could improve to 12% in FY27 compared to a likely 10.5-

11% in FY26 and 11% during FY24 and FY25. This should at

least drive a nominal GDP growth higher to 10- 11% in

FY27. As the profit accruals of corporates stay strong,

household credit growth could likely outpace the

corporate credit growth.

Exhibit 27

Bank credit growth and aggregate credit growth

Source: CMIE, RBI, SBIFM Research

Source: CMIE, RBI, SBIFM Research

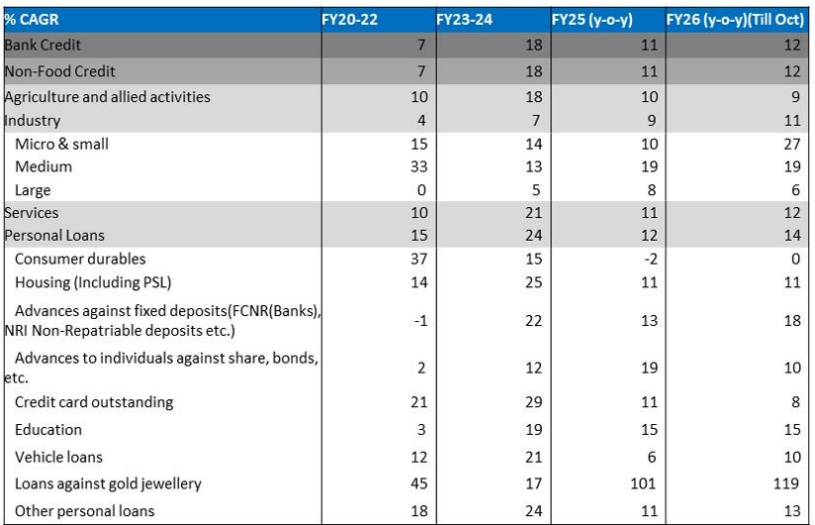

Exhibit 28

Break-up of bank credit

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

A pick-up in credit, contained inflation, government

supportive measures along with a decent income backdrop

should aid consumption recovery

Constructive outlook on FY27 consumption; Segments

thriving on credit-led demand could outperform

We remain optimistic about consumption demand in FY27,

supported by stronger credit flows, contained inflation,

and the sustained impact of multiple government

initiatives. While personal loan growth was robust in

FY23 and FY24 (21% and 28%, respectively), consumption

remained muted as credit was largely used to offset

COVID-induced income stress. This time, with a healthier

income backdrop, improved credit availability is

expected to translate into stronger consumption.

Segments that thrive on credit-driven demand could

perform particularly well in FY27.

Rural spending outlook positive as welfare measures and

low inflation mitigate kharif income setback

Further, state welfare schemes, combined with easing

inflation and improving wage growth, have boosted rural

consumer sentiment (Exhibit 29 to 32). The welfare

schemes primarily target women, farmers, senior

citizens, and the unemployed, with free or subsidized

electricity and LPG are also becoming widespread. 14

states are offering unconditional cash transfers to

women in FY26. While it is often argued that these

schemes merely reallocate revenue expenditure and hence

are not truly income supportive. However, we think that

they represent direct cash transfers and carry

significant political visibility, making

non-implementation difficult. Hence, even as there has

been a mere rejuggling of revenue expenditure, this is

more direct in nature and enables better cash inflow to

low-income households (Exhibit 33 to 35).

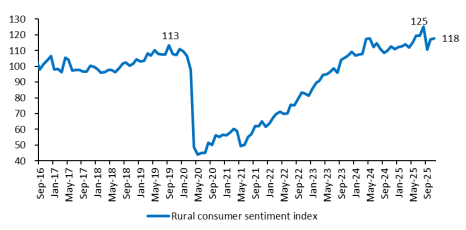

Exhibit 29

CMIE Rural consumer sentiment index is healthy

Source: CMIE Rural consumer sentiment index

is healthy

Source: CMIE Rural consumer sentiment index

is healthy

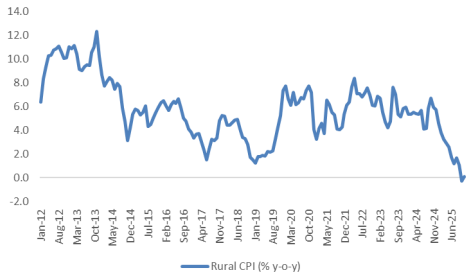

Exhibit 30

Rural CPI inflation is at an all-time low

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

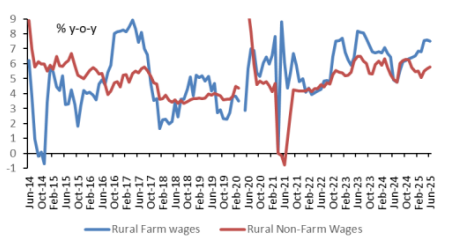

Exhibit 31

Rural wage growth sees modest improvement

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

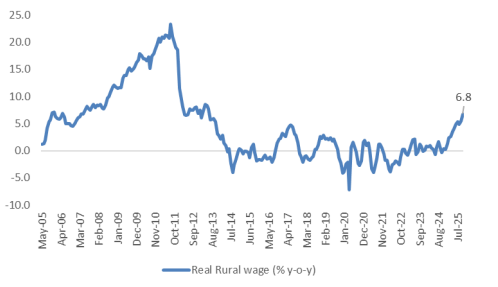

Exhibit 32

Wage growth in real terms is at the highest level

since 2013

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 33

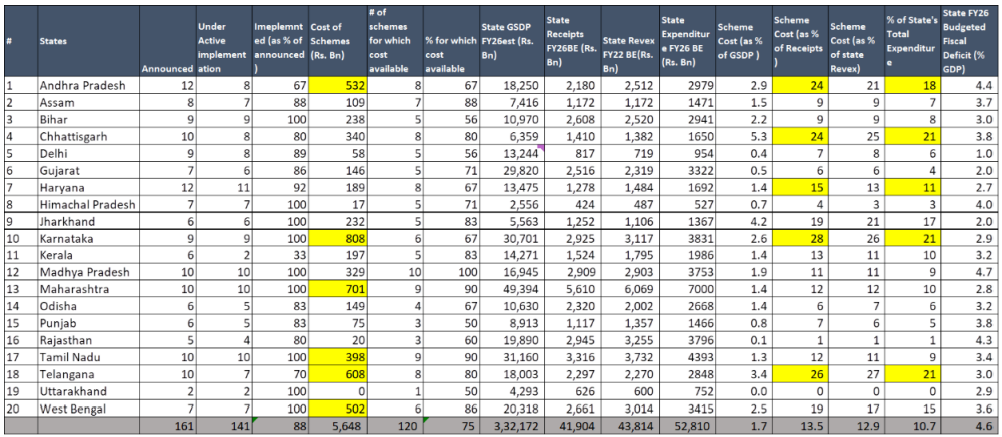

Welfare schemes account for 11% of expenditure and

13.5% of receipts across states; High welfare outlay

in Andhra Pradesh, Karnataka, Maharashtra, Tamil Nadu,

Telangana, West Bengal

Source: State budget documents, media

resources, CMIE, SBIFM Research

Source: State budget documents, media

resources, CMIE, SBIFM Research

Exhibit 34

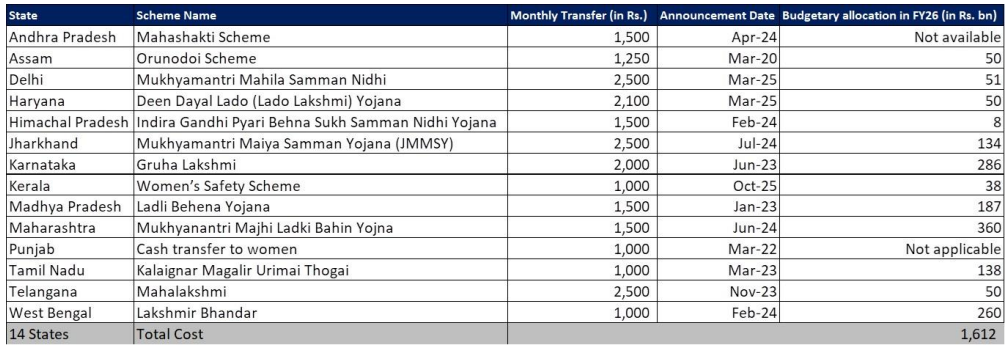

4 States have monthly income transfer schemes for

women ranging from Rs. 1000-2500 per month; entails an

annual cost of Rs. 1.6 trillion

Source: State budget documents, media

resources, SBIFM Research

Source: State budget documents, media

resources, SBIFM Research

Exhibit 35

States rejig revenue expenses to accommodate the

welfare expenses

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

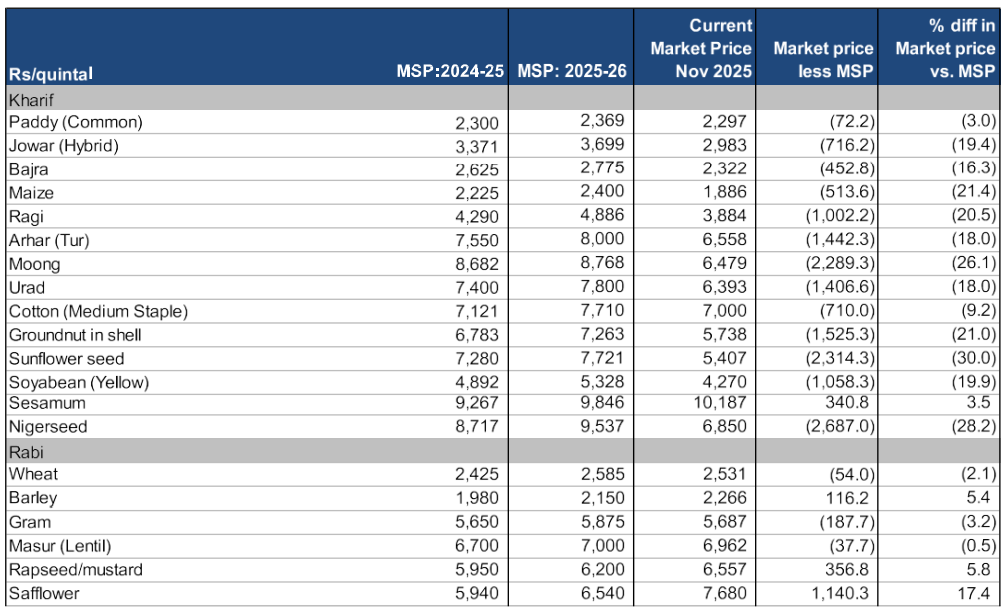

Yet, one adverse development stands out: Kharif income

has weakened this season due to unseasonal rains

affecting yields, especially for oilseeds and pulses.

Despite strong inventories, prices have fallen below

MSPs for most food grains, even compared to last year’s

MSP levels (Exhibit 36,37,38). While farmers may

withstand one weak season after two bumper years,

sectors reliant on farm income—such as two-wheelers,

fertilizers, and tractors—could face headwinds.

Encouragingly, Rabi sowing is progressing well.

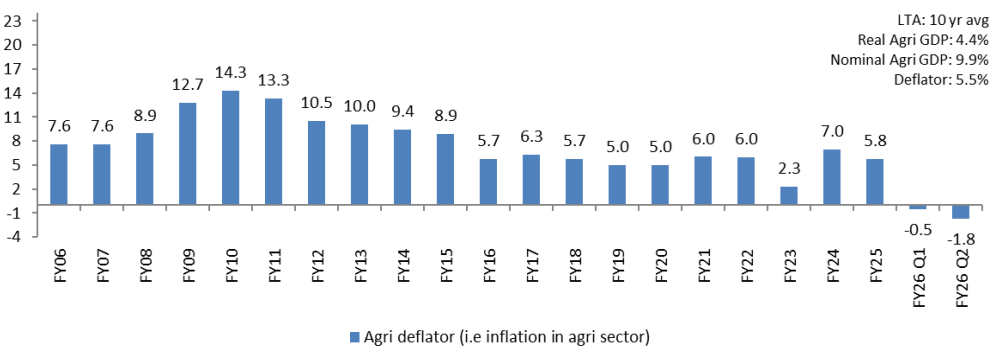

Exhibit 36

Agri and allied income growth one of the lowest since

FY06.

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 37

Sharp decline in agri prices in FY25-26

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 38

Prices of all the crops are trading below their MSP.

For Kharif crops, their current prices are even below

2024 MSP

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Urban consumption outlook: cautious but improving

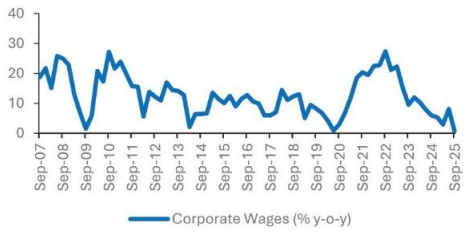

Urban households have faced headwinds from moderating

corporate wages and reduced hiring in banks and IT since

FY25. However, if overall economic growth strengthens,

hiring activity should pick up, improving the outlook

for urban consumption demand.

Exhibit 39

Corporate wage growth

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 40

Hiring falls in financial sector and IT

Source: Ace Equity, Capitaline, SBIFM

Research

Source: Ace Equity, Capitaline, SBIFM

Research

Premiumization: a structural consumption theme

While we often bucket consumption trends into rural and

urban segments, one theme stands out as a structural

play—premiumization. Rising middle-class incomes,

demographic dividends, a large population base, and

growth outpacing most global peers have provided a

strong backdrop for this trend. Premiumization of the

consumption basket is likely to remain a key driver in

the medium to long term.

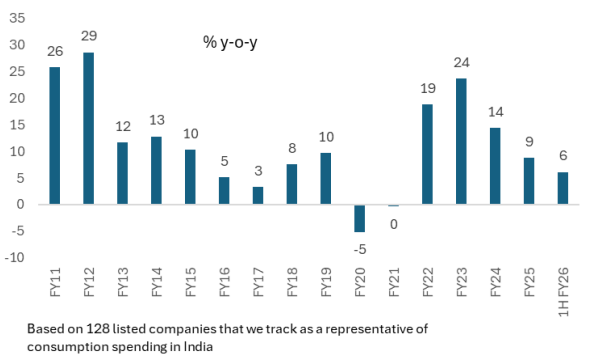

Exhibit 41

Consumption spending has been moderating since FY25

Source: Ace Equity, SBIFM Research

Source: Ace Equity, SBIFM Research

Consumption spending has been moderating since FY25 (E x

h i b i t 41). However, we find that segments associated

with premium consumption have depicted much stronger

growth (Exhibit 42).

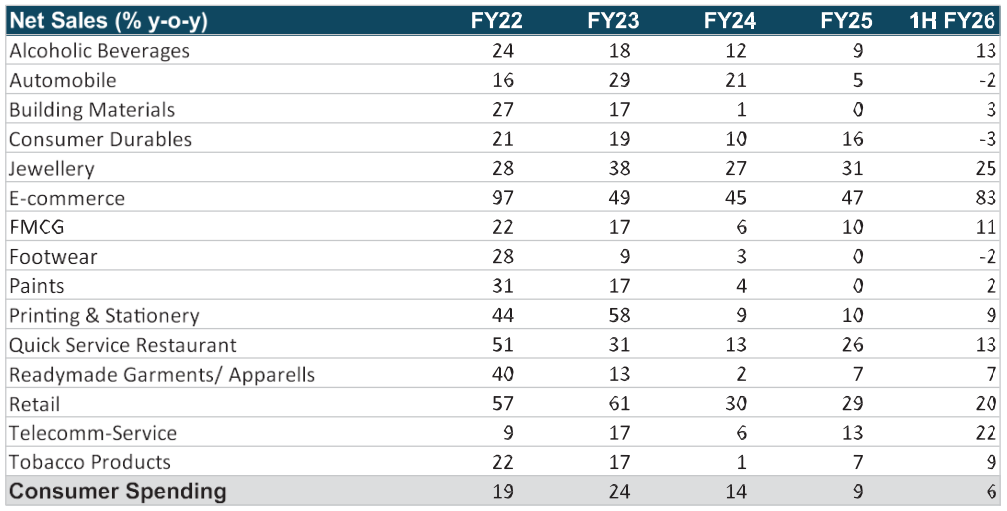

Exhibit 42

Stronger sales in Jewellery, E-commerce, QSR, Retail

and telecom relative to other sectors

Source: Ace Equity, SBIFM Research: NB: Based

on 128 listed companies that we track as a

representative of consumption spending in India

Source: Ace Equity, SBIFM Research: NB: Based

on 128 listed companies that we track as a

representative of consumption spending in India

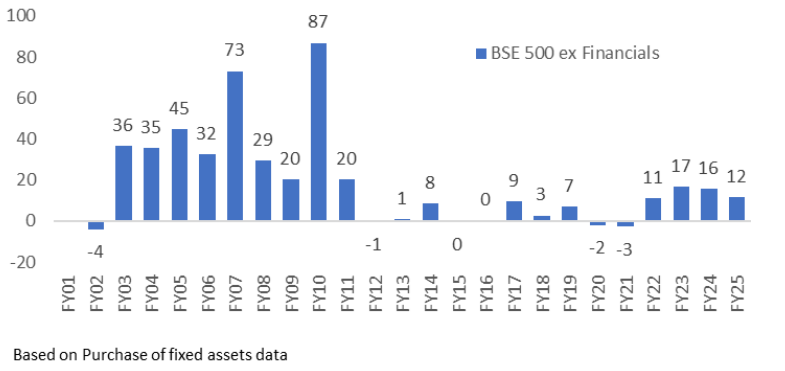

Corporate capex has been healthy

BSE 500 ex financials capex has expanded by 12% in FY25

vs. 16% in FY24 (Exhibit 43). Two third of the capex

comes from power and gas sectors. As per our assessment,

the capex growth has likely continued to be in mid-teens

in FY26 and will further expand by 10-12% in FY27. We

believe the real estate and power-generation cycles

remain in good health.

The capex outlook is also positive for renewables, data

centre, and cement sector in India. There is a vision to

increase data centre capacity from current 1-1.2GW to

3GW over the next four years which would entail a capex

outgo of Rs. 1-1.2 trillion over the period. A healthy

growth in the urban India housing (which accounts for

12-15% of cement demand) compared to an extremely muted

real estate activity for most part of last decade, is

the key factor driving a pick-up on cement demand and

there by capacity utilization while other segments of

demand continue to hold a healthy pace. While auto and

textile sector companies have retained the capex

guidance, if the India US trade deal stays stuck even in

2026, it could pose some downside risks to the capacity

addition in these sectors. On the other hand, capex

outlook for Oil & Gas, Chemicals and Sugar sector

appears weak owing to heavy capex activity in the oil &

Gas sector in recent years, the overhang of Chinese

dumping in the chemicals sector and completion of

sufficient ethanol plant addition in the sugar sector.

Exhibit 43

BSE 500: Capex activity shows double digit growth

since FY22

Source: Ace Equity, SBIFM Research

Source: Ace Equity, SBIFM Research

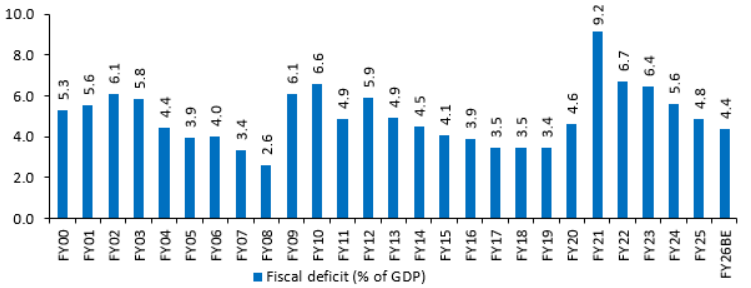

Central government capex commitment is likely to be in

line with Nominal GDP growth as the pace of fiscal

consolidation likely moderates

Over the past three years, the central government has

reduced its fiscal deficit by 2 percentage points—from

6.4% in FY23 to a likely 4.4% by FY26 (Exhibit 44).

Exhibit 44

Centre’s fiscal deficit

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Consequently, after a near tripling of capex outgo from

Rs. 3.3 trillion in FY20 to Rs. 9.5 trillion by FY24

(partly due to the absorption of off-balance-sheet capex

into the main budget), the strong infrastructure push

led by the central government has since cooled. We are

given to understand that more than the funding

constraints, execution challenges have been at the front

foot of moderating infrastructure activities in India

over last three years

Looking ahead in FY27, we do not expect any material

change in infrastructure outlook. On a positive note,

the pace of consolidation will likely come down to 20bps

in FY27. Better growth should drive an improvement in

tax buoyancy in FY27. We estimate Centre’s capex

commitment to be in line with Nominal GDP growth.

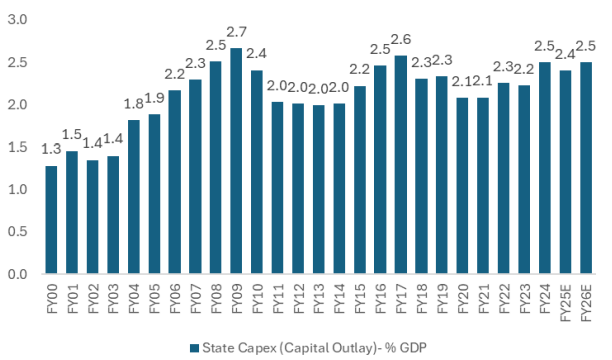

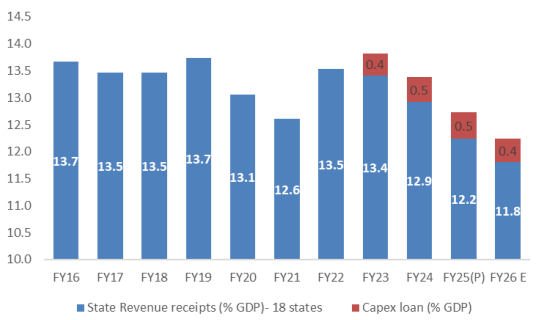

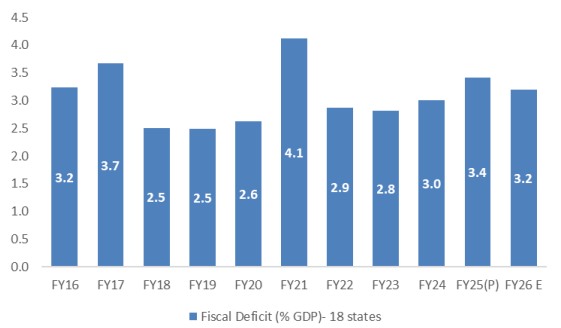

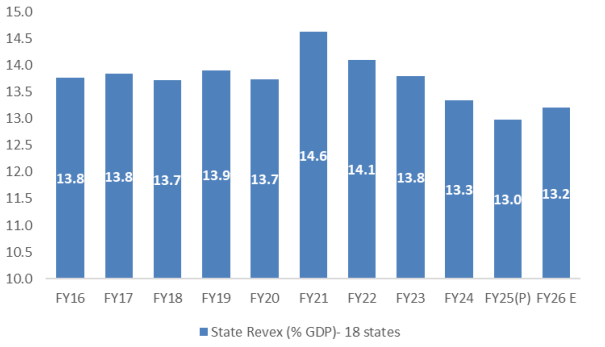

State capital outlay has been intact at 2.4-2.5% of GDP

While it is true that implementation of state welfare

schemes and lack of revenue buoyancy in states’ finances

has led to widening of state deficit from 2.5% of GDP

(FY18–FY20) to 3.2–3.5% in FY25–FY26, state capital

outlay has largely remained stable, ranging between 2.2%

and 2.4% of GDP from FY15 to FY25 (Exhibit 45).

This resilience is partly due to the 50-year

interest-free capex loans offered under the Scheme for

Special Assistance to States for Capital Investment

(SASCI) since FY21. These loans, outside the normal

borrowing limit, have grown from Rs. 120 billion in FY21

to an estimated Rs. 1,500 billion in FY26, financing 19%

of states’ capital outlay in FY25 compared to 2.9% in

FY21. While states’ own capital spending effort

(excluding SASCI loans) has remained relatively stable,

central assistance has given a boost to capital

expenditure. In 2024-25, several states have estimated

to finance more than 25% of capital outlay through these

loans.

Exhibit 45

State capex remains intact despite welfare spending

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

To sum it all, consumption demand appears to be the key

driver of improved growth in FY27 while the growth

momentum in corporate capex and infrastructure activity

could be similar to FY26. We are least constructive on

exports. Impact of any trade deal remains unclear for

now as competition from China is fierce and risks to

global growth and geopolitics continues to be a key

downside risk for FY27 too.

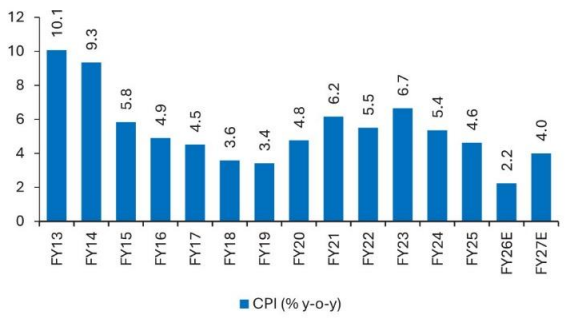

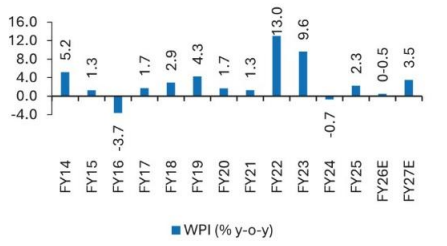

Inflation outlook: benign but rising in FY27

We expect inflation to average around 4% in FY27, up

from sub-2% levels likely in FY26—marking two

consecutive years below or at RBI’s 4% target. Inflation

is expected to move above 4% only by October next year,

largely due to base effects (Exhibit 46).

Exhibit 46

CPI outlook benign for FY27

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

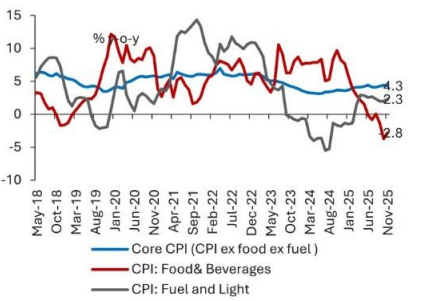

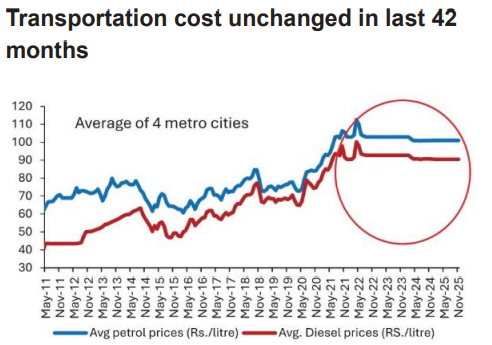

Cyclically, this benign inflation environment reflects

several factors: capped food inflation from continued

positive supply shocks, low commodity input costs,

moderating wage growth, and further transmission of GST

cuts to prices from October. Structurally, efficiency

and productivity gains from infrastructure investment

and increased digital transactions have also played a

role. Additionally, anchored inflation expectations

under the inflation-targeting regime, proactive

government supplyside measures, and heightened

competition from Chinese imports have contributed to

this trend (Exhibit 47 to 50).

Exhibit 47

Food inflation to likely mean revert in FY27

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 48

Transportation cost unchanged in last 42 months

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 49

Annual WPI inflation

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

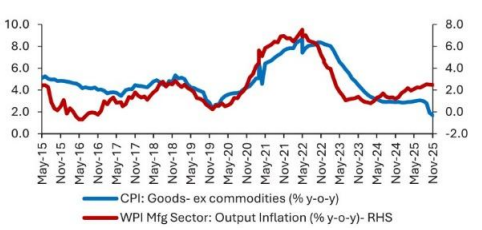

Exhibit 50

WPI inflation and CPI goods inflation correlated

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Monetary policy to stay supportive – liquidity actions

at the fore

While we would not rule out one more rate cut in 2026,

monetary policy in India is likely headed for a long

pause (unless global growth outlook deteriorates).

Liquidity, however, would continue to stay supportive

and we expect continued liquidity infusion into the

early parts of 2026

Centre on the path of modest fiscal consolidation; state

fiscal has deteriorated

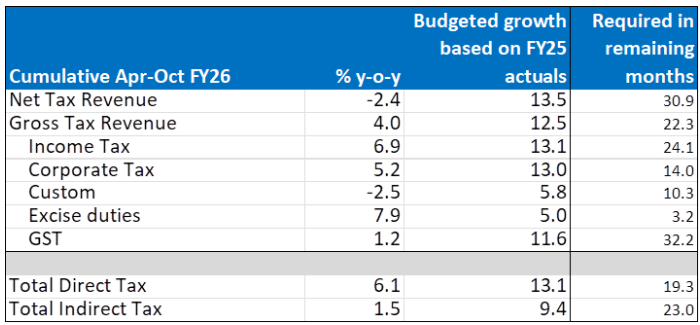

We expect Centre to stick to 4.4% of fiscal deficit

target in FY26. Direct tax collections improved in

October’25 (42% y-o-y) while indirect taxes declined

-5.7% y-o-y. Despite this, total 7M gross tax collection

has grown by 4% y-o-y. It is required to grow by 22% in

remaining 5 months to meet the budgeted targets (Exhibit

51). Indirect taxes could stay weak as GST effect also

creeps in 2H FY26. We estimate that overall tax revenue

could miss the budgeted target by Rs. 1.5 trillion. A

part of this will be offset by improved dividend

collection. Overall receipt shortfall is estimated at

0.2% of GDP which is manageable by minor expenditure

adjustment. We expect a modest consolidation to 4.2% of

GDP in FY27 implying a gross and net G-sec supply of Rs.

15.5 trillion and 11.5 trillion, respectively.

Exhibit 51

Gross tax collection likely to fall short of the

requited 22% in remaining 5M FY26 to meet budgeted

targets

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

On the other hand, state finances have been

deteriorating. State fiscal deficits have risen—from

2.5% of GDP (FY18–FY20) to 3.2–3.5% in FY25–FY26—amid

falling receipts and higher welfare spending (Exhibit

52, 53, 54). The RBI (2024) cautioned that rising

expenditure on subsidies and cash transfers to farmers,

youth, and women could strain state finances,

recommending rationalization to preserve space for

productive spending. Given that these schemes carry

significant political visibility, non- implementation

would be increasingly difficult. Further, there are

impending problems with multiple state DISCOMS too which

must be addressed sooner than later.

Exhibit 52

Despite capex loan, the flow of receipts to states has

moderated during FY24-26

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 53

Reduced receipts and welfare measures have driven

state deficit to 3.2-3.4% of GDP during FY25- FY26

from 2.8% during FY22-23 and 2.5% during FY18-19.

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Exhibit 54

So far, states are rejigging their revenue expenses to

accommodate the welfare expenses

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

Regulations and capex loan keep state borrowing under

check

Even as state fiscal deficits are rising, a part of this

is getting funded by Centre’s capex loan. Further,

regulatory limits on states’ borrowing have also helped

to keep overall state fiscal deficit in check and forced

states to rejuggle their expenses and accommodate the

rise in scheme-based expenditure.

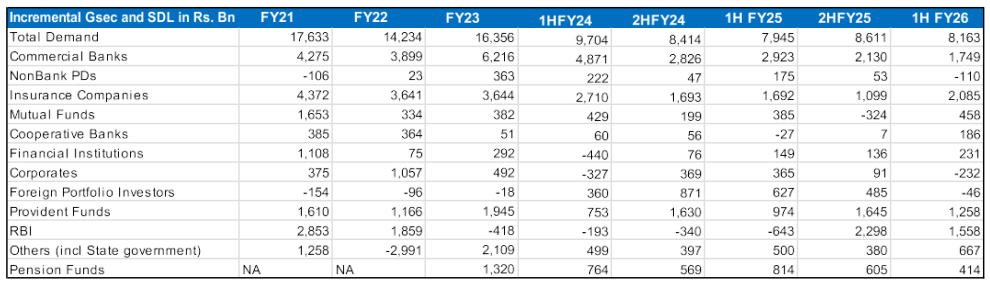

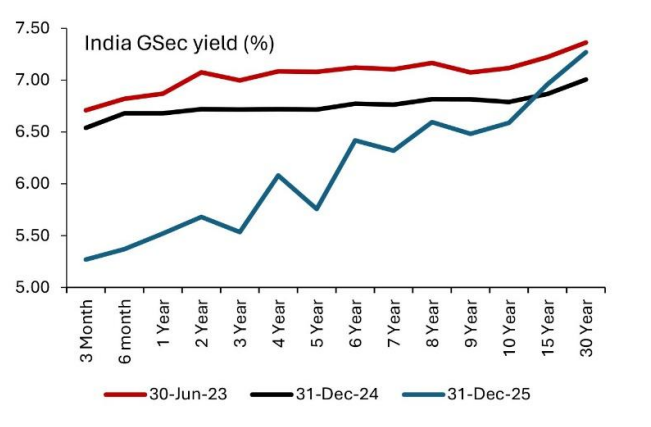

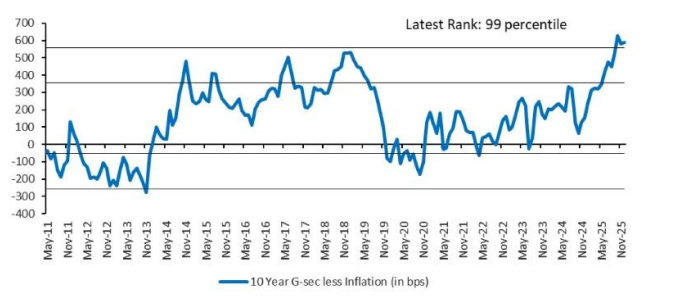

Government bonds supply could rise to Rs. 29 trillion in

FY27 (vs. Rs. 27.2 trillion in FY26)

In FY26, budgeted gross SDL had jumped by 16% to Rs.

12.4 trillion (most likely will go through). In FY27, we

expect net and gross SDL borrowing to rise to Rs. 9.5

trillion (vs. Rs. 8.7 trillion in FY26) and gross supply

to rise to Rs. 13.5 trillion. To sum, the overall supply

of government securities is estimated to rise to Rs. 29

trillion in FY27 against an estimated Rs. 27.2 trillion

in FY26.

Government bonds’ demand supply dynamics continues to

stay in a tight spot in FY27

Even as a likely inclusion of India in Bloomberg

Aggregate Index and resumption of NPS buying in FY27

appears to be a positive thrust, the demand supply

equation for government bond stays in a tight spot.

Improving credit growth in the banking system amid

elevated credit to deposit ratio would keep banks’ SLR

investment under check. Further, RBI has conducted Rs.

3.7 trillion of OMO purchase between Apr-Dec 2025 and

more could be in the offing in Q4 FY26. We are not sure

if liquidity dynamics would necessitate a similar OMO

action in FY27 (Exhibit 55).

Exhibit 55

Government bond demand supply

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

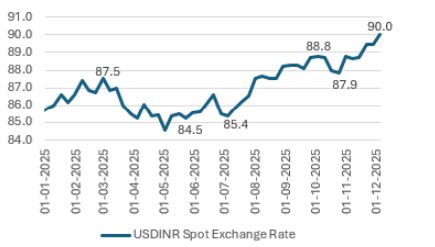

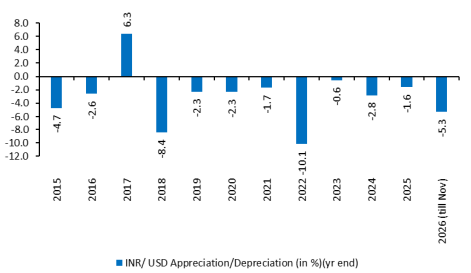

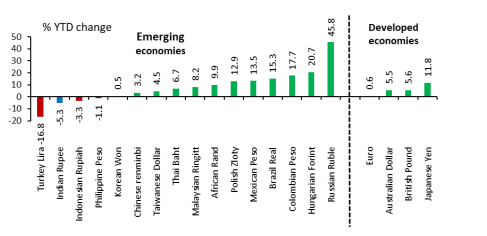

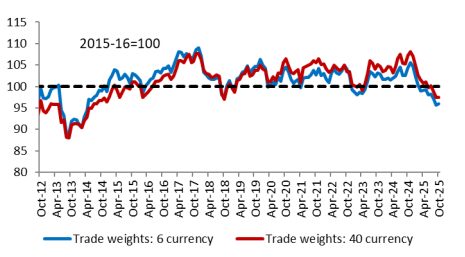

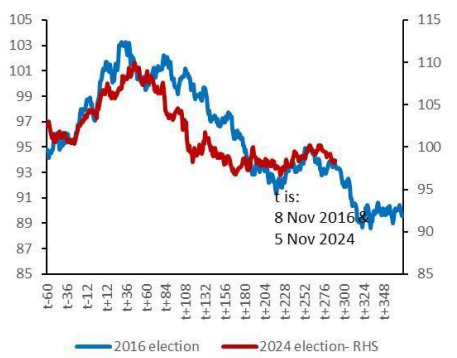

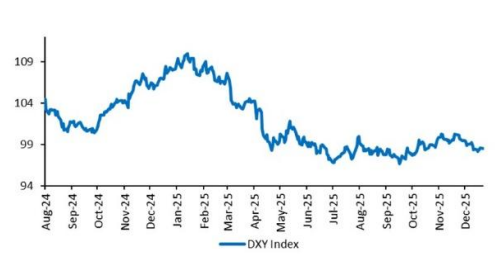

Rupee has been the focal point in 2025- depreciating

nearly 5% in 2025

The Indian rupee witnessed significant depreciation in

November, marking its sharpest pace of decline since

2022 (Exhibit 56 and 57). Interestingly, this weakness

has unfolded despite the U.S. dollar index (DXY) showing

an 8% decline and most emerging market currencies,

except Indonesia and Türkiye, appreciating against the

dollar. Typically, India’s lower inflation relative to

the U.S., stable crude prices, fiscal discipline, and

Current account deficit under 1% of GDP support Indian

assets and the rupee.

Exhibit 56

Rupee moves in 2025

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Exhibit 57

Sharpest depreciation in rupee since 2022

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Exhibit 58

Dollar on a weakening bias

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Exhibit 59

Rupee underperforms relative to EM peers

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

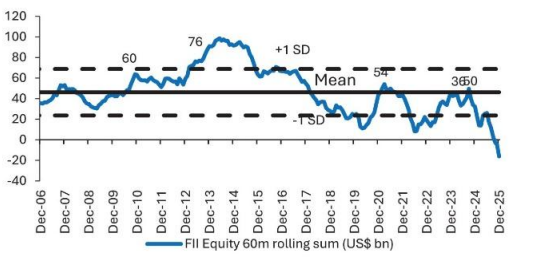

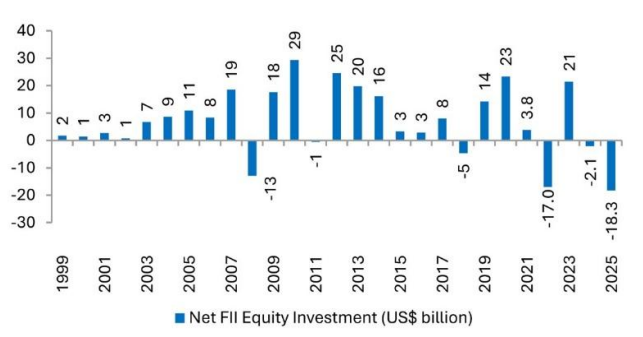

No trade deal at the helm of this mayhem

While India’s overall GDP growth appears to be largely

cushioned and minimally impacted by reduced exports to

the US, it is clearly impacting the external account and

hence sentiment around Rupee. Weak trade dynamics and

earnings downgrades are weighing on rupee sentiment.

Indian exports are up 4% y-o-y FYTD, while global

exports rise. FPI flows remain muted, owing to the

combination of earnings downgrades, lack of AI plays and

no positive developments around trade deal (Exhibit 60).

India’s MSCI weight has slipped to third place after

nearly overtaking China last year. Thus, India’s

external account struggle has been more on the capital

inflow side which has not been even enough to cover up

for this muted CAD.

Exhibit 60

FII outflow should see a turnaround in FY27

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

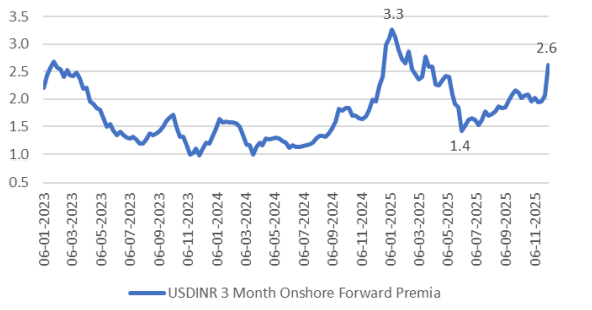

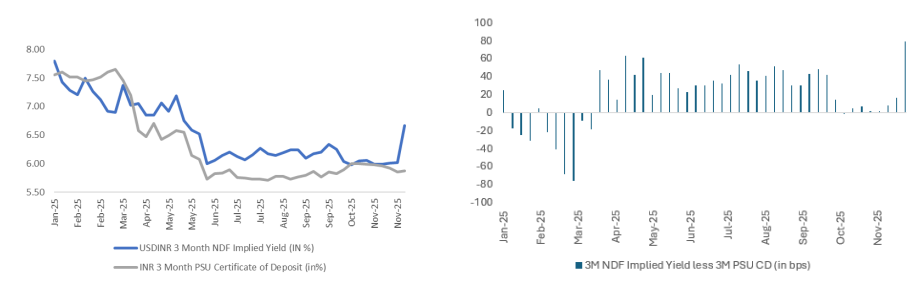

From Forward to Spot: Hedging Rush and Rising Premiums

Weakening sentiment around rupee triggered panic among

importers, prompting a rush to hedge future dollar

liabilities. This surge in hedging demand has pushed up

forward premiums in India. The 3-month dollar forwards

premium now stands at 2.6%, up from 1.4% six months ago

(Exhibit 61). Consequently, 3M INR implied yield (i.e.,

selling rupee and investing in dollar adjusted for the

hedging cost) offer an annualized return of roughly 6.70

%, (vs. 6% six months ago) compared to Indian PSU CDs

yielding 6.05% for similar tenors (CDs have been at

similar levels since Jun’25). This 90bps differential

effectively caps downward adjustment in onshore short

end rupee assets (Exhibit 62). To add, relaxation in RBI

rules are also leading exporters to delay in

repatriating their dollar earnings back to India.

Exhibit 61

Dollar forward premia jumps

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Exhibit 62

Sharp arbitrage opportunity between Indian CD’s and

NDF Implied yield

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

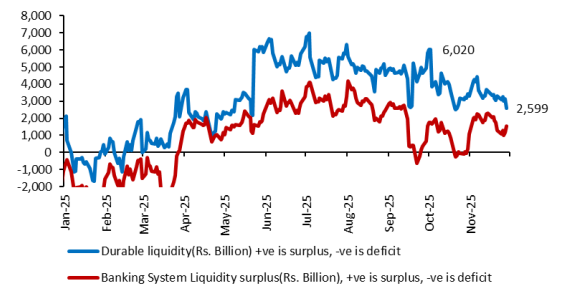

Exhibit 63

Banking System liquidity falls substantially due to

dollar capital outflow

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Impact on Domestic Markets

The dollar squeeze has led to increased selloffs in

Indian assets, reduced INR liquidity in the system, and

a rise in buy-sell swaps by private players. Forward

market stress is spilling over into spot rates because

of arbitrage opportunities. Despite a 100bps CRR cut

during September to Nov’25, durable banking system

liquidity has fallen from 5-6 trillion during July’25 to

2.6 trillion by end November (Exhibit 63).

At equilibrium, returns on rupee assets equal returns on

dollar assets plus hedging cost. Currently, rupee

returns are lower than this benchmark, creating

persistent pressure. To restore balance, one of the

following must occur: U.S. Treasury yields decline,

hedging costs fall, or Indian fixed-income yields rise.

This is partially happening. Despite a 25bps repo rate

cut and a Rs.1.45 trillion-rupee liquidity injection

announced in December MPC meet, Indian yields have

firmed. 10-year G-sec is up 10–12bps and three-month CDs

up 15–16bps. Thus, monetary easing since June has not

led to similar transmission in market rates (despite an

ultra-low inflation). Position unwinding by FPI’s

(reducing EM risk) leading to rise in offshore NDOIS

spilling over to onshore swaps have led to up move in

domestic yields, particularly since November. At the

same time, the market continues to grapple with Rupee

dynamics, alongside weak demand for sovereign assets due

to regulatory and taxation changes.

A durable solution requires either a meaningful shift in

rupee sentiment or RBI intervention via continued OMO

purchases. Our assessment suggests RBI may need to

inject an additional Rs. 2 trillion rupees over the next

three months to maintain LAF near 1% of NDTL. Now the

currency woes suggest that these liquidity actions could

come increasingly in the form of buy sell swap rather

than OMO purchases. This has been another reason to lead

to some adverse movement in G-sec yields in past one

week.

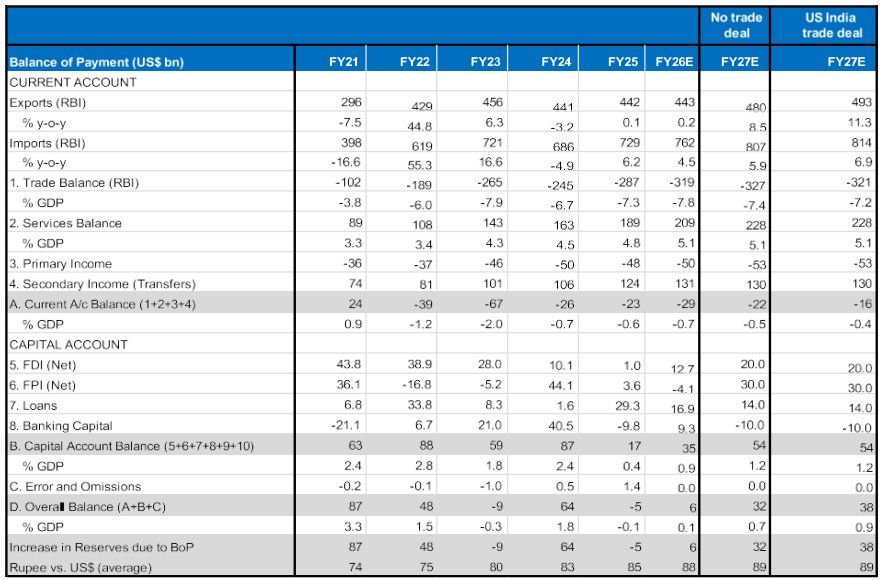

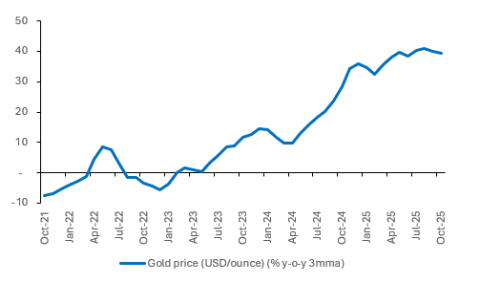

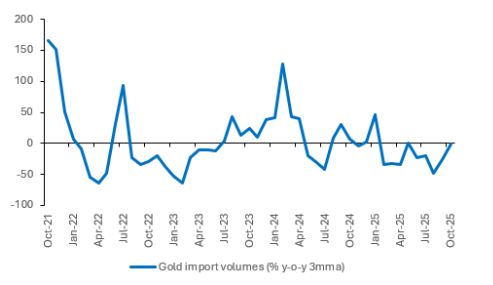

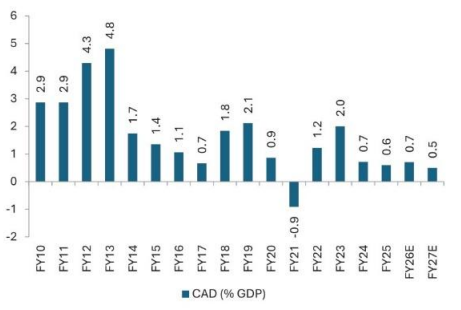

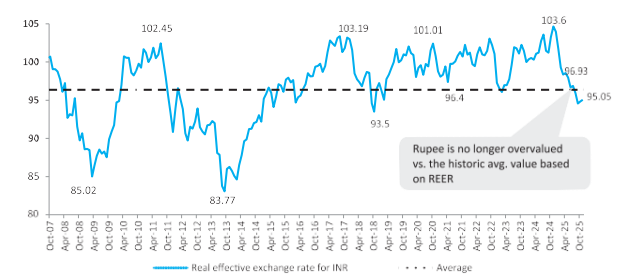

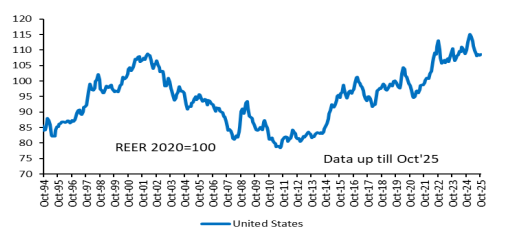

We are not meaningfully worried on Rupee

The INR’s recent weakness despite low inflation has

brought the REER to competitive levels. We do not see an

unduly stressed Balance-of-Payments. The impact of the

surge in investor demand for gold, which is keeping

import volumes high despite 50% higher prices is offset

by weak oil prices. A higher non-oil/gold deficit due to

a recovering economy and Chinese competition in export

markets can be paid for by the continuing double-digit

growth in net services exports. We expect the current

account deficit to stay contained under 1% of GDP in

FY26 and FY27. More importantly, we expect capital

inflow to improve in FY27 on the hopes of India’s

inclusion in another global bond indices. Further

overall FPI inflows in equity has reached to a level

where one can expect some resumption in equity purchases

by the foreigners. To sum, after ~5% depreciation in

2025 and ~4% depreciation FYTD, we expect rupee to

depreciate by a mere 2% in FY27 (i.e., 92/US$). In case

of a trade deal, we would not be surprised if Rupee

appreciates around the deal announcement (Exhibit 64 to

70).

Exhibit 64

BoP Outlook

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Exhibit 65

Trade deal has had a significant impact on India’s

exports;

Source: CMIE Economic Outlook, SBIFM

Research

Source: CMIE Economic Outlook, SBIFM

Research

Exhibit 66

Outlook for services exports stay healthy

Exhibit 67

Gold prices rose sharply leading to gold import

volumes being subdued

Source: CMIE Economic Outlook, SBIFM

Research

Source: CMIE Economic Outlook, SBIFM

Research

Exhibit 68

Outlook for services exports stay healthy

Exhibit 69

CAD to remain contained at under 1% of GDP for

FY26 and FY27

Source: RBI, CMIE Economic Outlook, SBIFM

Research

Source: RBI, CMIE Economic Outlook, SBIFM

Research

Exhibit 70

INR REER is 5% below the fair value

Source: CMIE, SBIFM Research

Source: CMIE, SBIFM Research

acfb44ed30d547d09bfedd904c194828)

0bf21f855da944d2a0c843c4553297d8)

Source: Bloomberg, SBIFM Research; NB: Taiwan

and Philippines have seen material revision in their

2025 growth outlook; India data for FY26 is RBI’s

projection on financial year basis; FY27 is SBIFM

estimate

Source: Bloomberg, SBIFM Research; NB: Taiwan

and Philippines have seen material revision in their

2025 growth outlook; India data for FY26 is RBI’s

projection on financial year basis; FY27 is SBIFM

estimate

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source : Yale Budget Lab, Bloomberg, SBIFM

Research

Source : Yale Budget Lab, Bloomberg, SBIFM

Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source Bloomberg, SBIFM Research, Forecasts

are Bloomberg estimates

Source Bloomberg, SBIFM Research, Forecasts

are Bloomberg estimates

Source: Bloomberg, SBIFM Research; NB: Data

above reports y-o-y GDP instead of usually

referred to q-o-q SAAR

Source: Bloomberg, SBIFM Research; NB: Data

above reports y-o-y GDP instead of usually

referred to q-o-q SAAR

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research; NB: Red

denotes rate hike and green denotes rate cut

Source: Bloomberg, SBIFM Research; NB: Red

denotes rate hike and green denotes rate cut

Source: Bloomberg, SBIFM

Source: Bloomberg, SBIFM

Source: Bloomberg, SBIFM Research; NB:

Interest rate differential is the US vs. the

economies that make up DXY index, German Bund is

taken as a proxy for Euro

Source: Bloomberg, SBIFM Research; NB:

Interest rate differential is the US vs. the

economies that make up DXY index, German Bund is

taken as a proxy for Euro

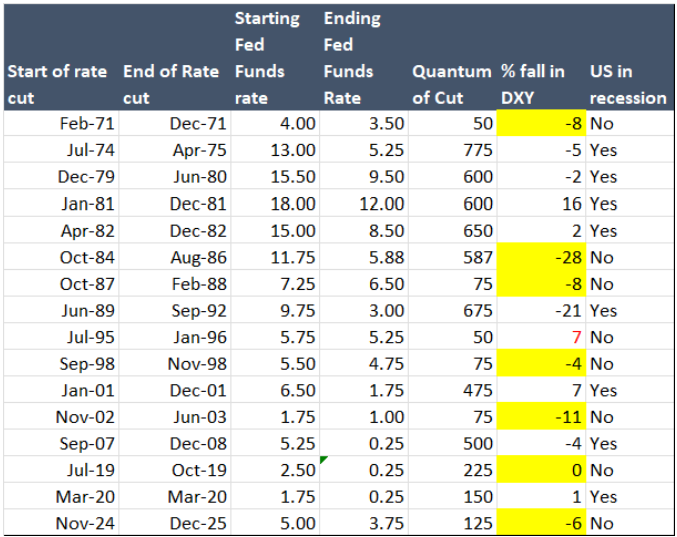

Source: Bloomberg, SBIFM Research; NB: Cells

highlighted depict depreciation in DXY when Fed cut

interest rates outside of the US recession

Source: Bloomberg, SBIFM Research; NB: Cells

highlighted depict depreciation in DXY when Fed cut

interest rates outside of the US recession

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

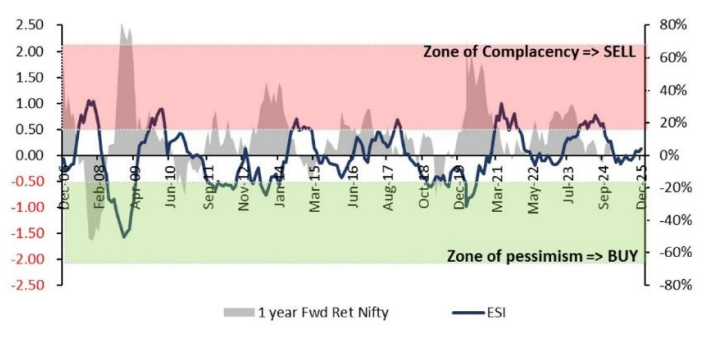

Source: Bloomberg, FactSet, SBIFM Research, ESI

stands for Equity Sentiment Index, our proprietary

equity sentiment measure

Source: Bloomberg, FactSet, SBIFM Research, ESI

stands for Equity Sentiment Index, our proprietary

equity sentiment measure

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: FactSet, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

Source: RBI, SBIFM Research

)

)