The return of an old problem

The inflation surge that began in 2022 has revived a debate many believed had been settled decades

ago. Central banks

initially characterised inflation as transient, shaped by temporary supply disruptions. Yet, as

price pressures proved more

persistent, the episode began to resemble earlier periods of sustained inflation. In particular, the

parallels with the 1970s have

become increasingly difficult to ignore.

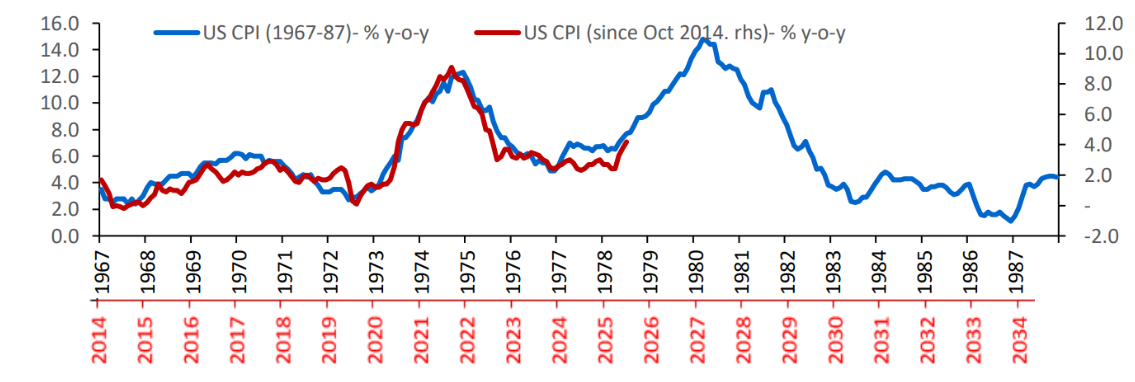

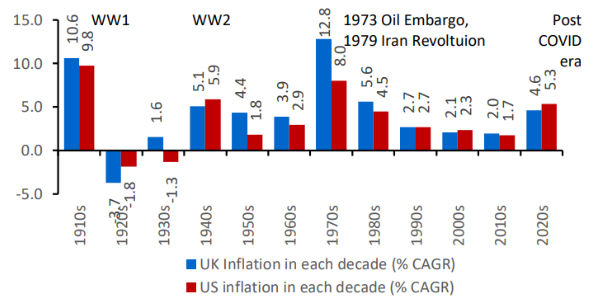

History suggests that inflation rarely arrives as a single, isolated shock. Instead, it tends to

emerge in waves. The 1970s

witnessed two distinct inflation episodes— the first in 1973–1974 and the second in 1979. (Exhibit

1). The possibility that

today’s cycle could follow a similar pattern—potentially culminating in a second wave later in the

decade—raises important

questions for policymakers and investors alike. If history repeats, investors must position

themselves in inflation-resilient assets

such as commodities, gold, and energy.

Exhibit 1: That 70s Show: Fears of a second wave of inflation

Source :

St Louis Fred, Bloomberg, SBIFM Research

Source :

St Louis Fred, Bloomberg, SBIFM Research

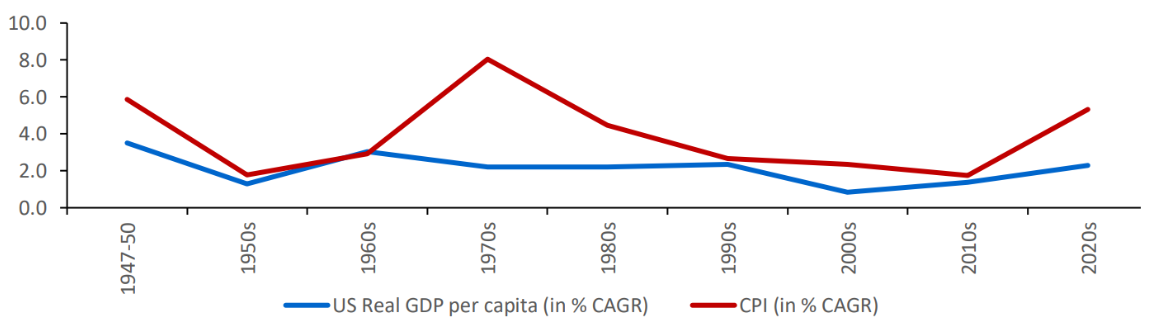

At its core, inflation is not merely about rising prices. It is about the erosion of the value of

money. Periods of sustained inflation

are typically those in which monetary conditions cease to act as an anchor. When that anchor

weakens, price pressures can

become entrenched, regardless of their initial source. Moderate inflation is considered necessary to

avoid deflation, which can

lead to excessive saving and economic stagnation. Historical data shows a positive correlation

between moderate inflation and

real GDP per capita growth, suggesting a healthy inflation range exists. However, rapid inflation

erodes purchasing power and

destabilizes economies (Exhibit 2). Central banks, therefore, aim to anchor inflation at moderate

levels, traditionally around 2%

in developed economies, though the optimal level remains debated.

Exhibit 2: Hyperinflation leads to erosion in purchasing power

Source : Bloomberg, St. Louis Fred, SBIFM Research, Data till Q1 2026

Source : Bloomberg, St. Louis Fred, SBIFM Research, Data till Q1 2026

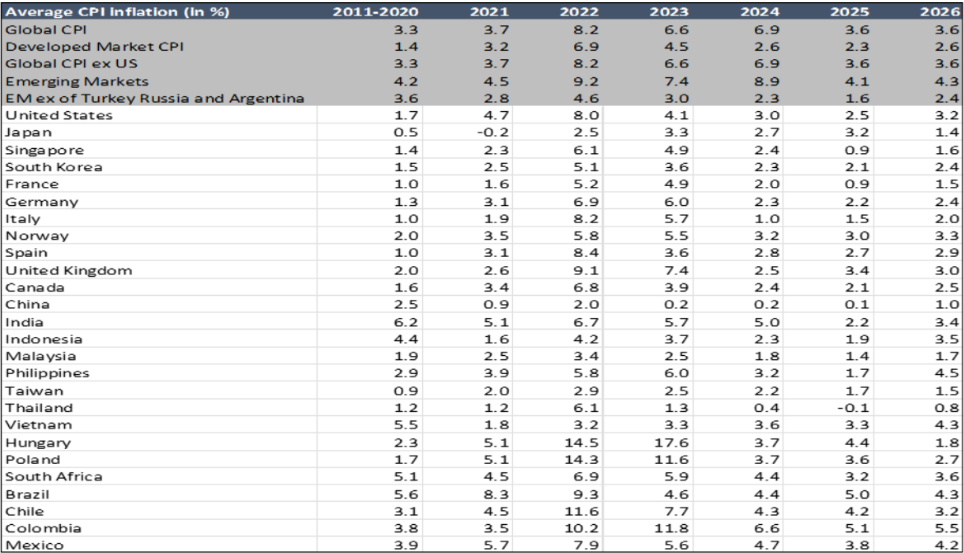

Global inflation trends: Post-COVID divergence

Post-pandemic inflation was widespread and largely supply-driven,

exacerbated by US monetary policy. However, while many

economies returned to pre-COVID inflation levels, several developed markets—including the United

States, Japan, and much

of Europe—continue to experience elevated inflation. Emerging markets like Turkey, Argentina, and

Russia also show high

inflation, but these are attributed to country-specific factors. In contrast, inflation in emerging

market ex of these economies has

moderated from a historical average of 3.6% during 2011-2020 to 2.4%, while developed markets have

seen their inflation

average increase by about 1.2% pt from a pre-COVID baseline of 1.4% (Exhibit 3).

Exhibit 3: Inflation surge across developed markets while emerging

market inflation are relatively

contained

Source : CEIC, SBIFM Research

Source : CEIC, SBIFM Research

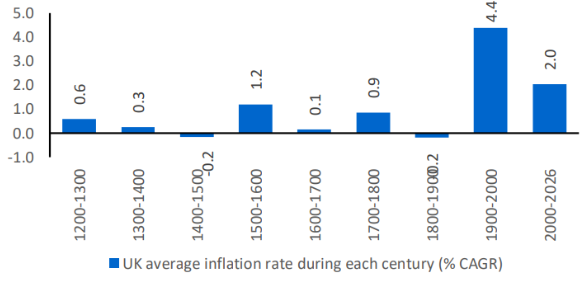

A monetary lens on inflation

A long-term historical perspective reveals that episodes of persistent

inflation have been relatively uncommon. For extended

stretches of history, particularly under metallic monetary systems, the purchasing power of money

remained remarkably stable.

The major exceptions occurred when monetary anchors weakened or disappeared. The influx of precious

metals from the New

World into Europe during the sixteenth century triggered one such episode (Exhibit 4). A sudden

increase in the stock of silver

expanded purchasing power faster than available production, generating a broad rise in prices across

the continent.

The nineteenth century marked a contrasting experience. Many economies

increasingly tied their monetary systems to gold or

silver standards, effectively limiting the ability of governments and financial systems to expand

money supply at will. At the

same time, industrialisation and technological advances increased productive capacity. Since output

grew more rapidly than

the monetary base, prices often exhibited a tendency towards stability or even mild declines. In

this environment, money

preserved its value over long periods.

The twentieth century represented a profound break from this historical

pattern. The collapse of commodity-backed monetary

systems and the widespread adoption of fiat currencies transformed the relationship between money

and prices. Governments

and central banks gained greater flexibility to expand money supply in pursuit of economic and

political objectives. While this

flexibility supported economic growth and helped manage financial crises, it also contributed to

repeated inflationary episodes.

Over the century, the cumulative decline in the purchasing power of money was unprecedented compared

with earlier eras.

Importantly, inflation has rarely emerged solely because of isolated

price shocks. While events such as commodity shortages,

wars or energy crises often act as a catalysing force, historical evidence suggests these factors

become persistently inflationary

only when accommodated by loose monetary conditions (Exhibit 5 & 6).

Exhibit 4: Inflation through history – a long-term

perspective

Source : Consumer Price Inflation in the United Kingdom (CPIIUKA) |

FRED | St.

Louis Fed

Source : Consumer Price Inflation in the United Kingdom (CPIIUKA) |

FRED | St.

Louis Fed

Exhibit 5: A closer look at 20th century inflation cycles

Source: Consumer Price Inflation in the United Kingdom (CPIIUKA) | FRED

| St.

Louis Fed, Bloomberg, SBIFM Research

Source: Consumer Price Inflation in the United Kingdom (CPIIUKA) | FRED

| St.

Louis Fed, Bloomberg, SBIFM Research

A misread of the history: Inflation in 1970s

The recent inflation episode is often described as supply-driven, linked

to pandemic disruptions, geopolitical fragmentation, and

energy shocks. While these factors clearly played a role, history cautions against placing too much

emphasis on proximate

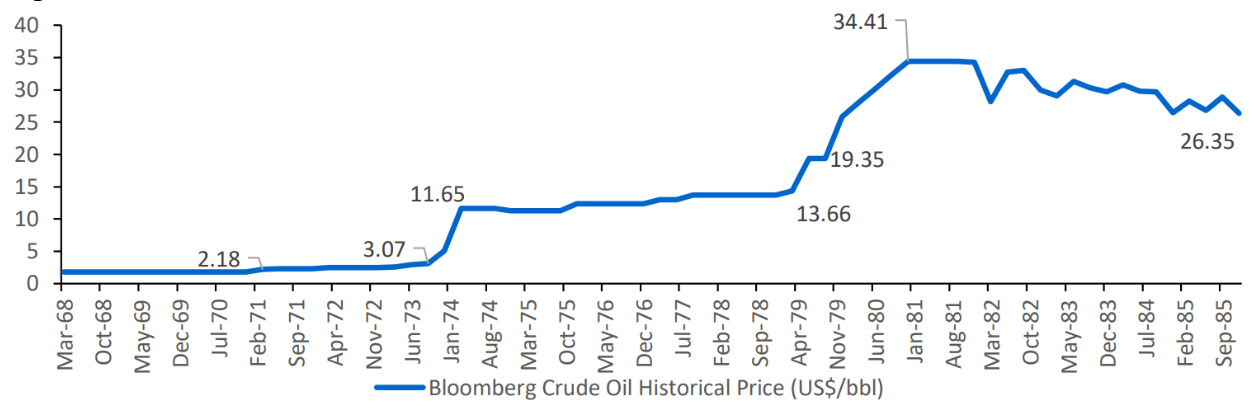

causes. The experience of the 1970s illustrates this clearly. Oil price shocks are widely viewed as

the trigger for inflation during

that period:

a) 1973 oil shock: Triggered by the Yom Kippur War and an oil embargo,

prices rose from ~$3 to ~$12 per barrel (Exhibit 7).

b) 1979 oil shock: Caused by the Iranian Revolution, prices jumped from

~$14 to ~$34 per barrel (Exhibit 7).

However, closer examination shows that inflation had already been rising

before oil prices surged. The oil shocks acted as

accelerants, not root causes.

What ultimately sustained inflation was an environment of excessively

loose monetary policy, strong demand, and rising wages.

In other words, inflation persisted not because of the shock itself, but because the underlying

monetary and economic conditions

allowed it to do so.

This distinction is crucial. Inflation can have many immediate

triggers—energy prices, supply bottlenecks, or fiscal stimulus—

but its persistence is typically a function of monetary conditions. As centuries of data suggest,

inflation is fundamentally a

monetary phenomenon.

Exhibit 7: A misreading of history: the 1973 and 1979 oil shocks were

accelerants, not the root cause of inflation

surge

Source :

Bloomberg, SBIFM Research

Source :

Bloomberg, SBIFM Research

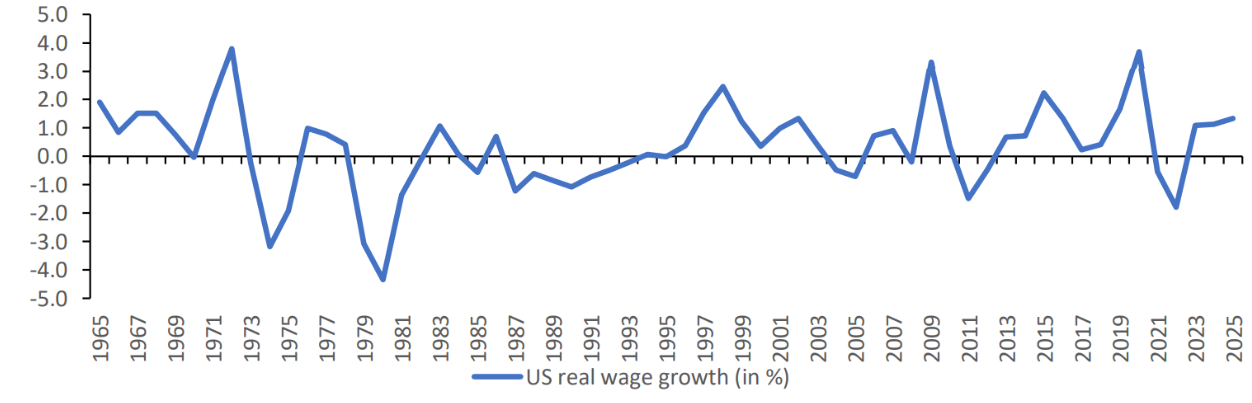

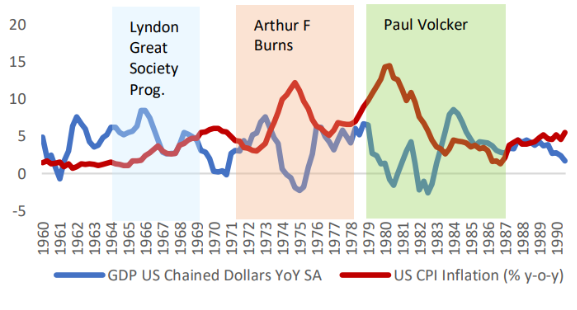

Real wage growth and policy focus on growth

In the US, real wage growth from 1965 to 1971 averaged 1.5–2%, indicating strong labour demand

(Exhibit 8). This was driven

by Lyndon Johnson’s “Great Society” programs aimed at full employment and growth. Today, similar

growth-focused narratives-Trump’s “Make America Great Again” and Biden’s “Build Back Better”-

suggest a parallel emphasis on expansionary policies.

Exhibit 8: Real wage growth was consistently positive from 1965- 1972

Source :Bloomberg, SBIFM Research

Source :Bloomberg, SBIFM Research

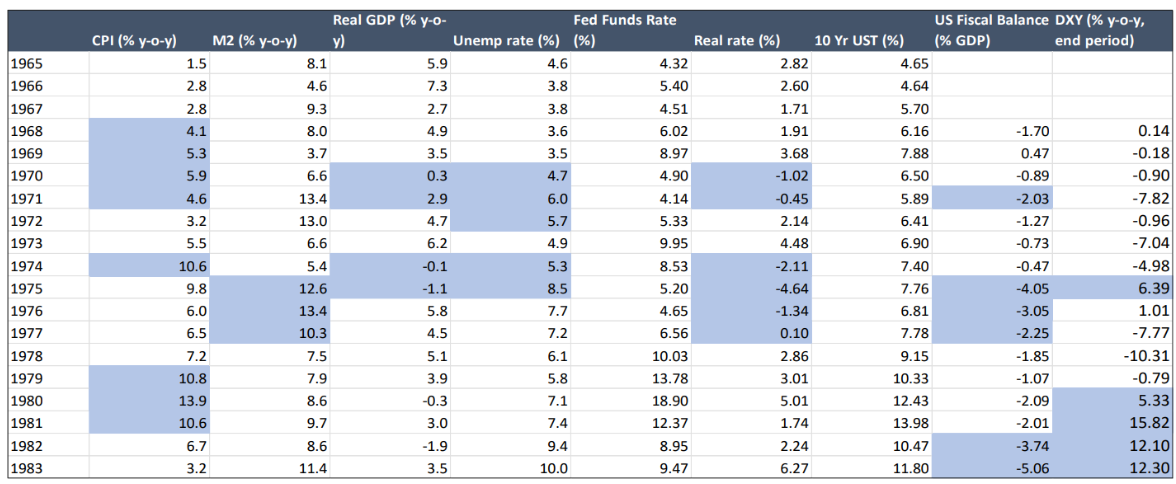

Inflation was already rising before the 1973 oil shock

Crucially, US inflation had already risen from 2.8% in 1967 to 5–6% by

1970, before the oil shock (Exhibit 9). This early rise

signalled the emergence of stagflation—rising inflation alongside slowing growth. Growth collapsed

from ~5% in 1968 to near

zero in the 1970, undermining the traditional Phillips Curve relationship.

Policy misdiagnosis

One of the defining features of the 1970s was the misdiagnosis of

inflation by policymakers. At the centre stage of this, are the

economies like US and UK. Central banks in these two large economies viewed inflation largely as a

cost-push phenomenon,

driven by wages, commodity prices, or external shocks. This led to a misplaced reliance on

administrative measures such as

wage and price controls rather than appropriate monetary tightening.

The consequences were severe. Real interest rates remained negative for

prolonged periods (Exhibit 9), allowing inflationary

pressures to build. At the same time, political pressures undermined central bank independence,

further delaying the required

policy response.

Milton Friedman’s view- “inflation is always and everywhere a monetary

phenomenon”- was ignored until the late 1970s.

Policymakers blamed bad weather, food shortages, unions, corporate greed, and OPEC, but not money

supply. A major error

was the misjudgement of the output gap. Policymakers believed the economy was operating below

capacity, justifying

expansionary policy. Later analysis showed this was wrong. Similarly, inflation expectations were

slow to adjust.

Finally, by 1979, importance of monetary actions was brought back to the

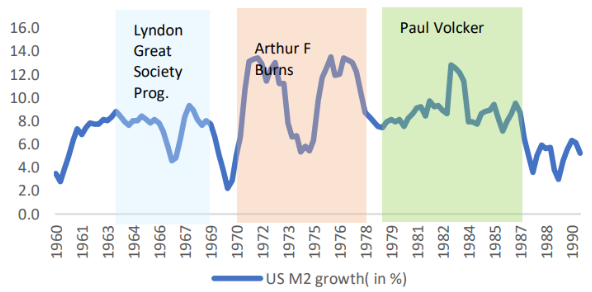

table. M2 growth slowed sharply in 1978 from its high

rates of 1976 and 1977; while policymakers in 1978 allowed nominal interest rates to rise by more

than the increase in the

current year’s inflation rate. The turnaround in monetary policy that produced the early 1980s

disinflation began in 1978. This

led to a recession but broke the back of inflation by 1982–1983 (Exhibit 9).

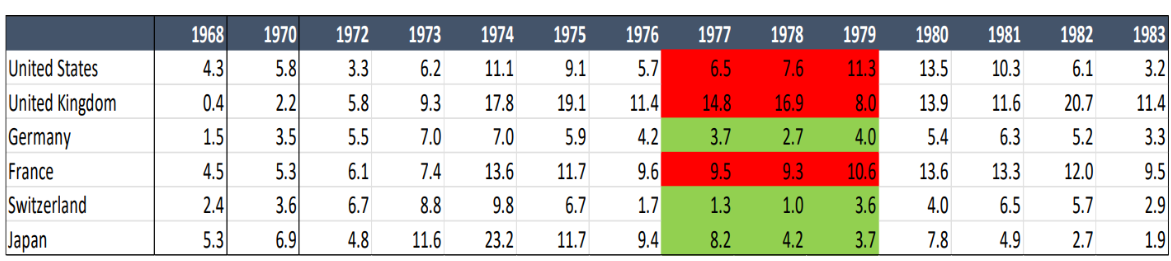

Exhibit 9: US macro indicators (1965–1983): US Fed did not respond

vigorously to the outbreak of inflation

Source : Bloomberg, SBIFM Research; NB: Coloured cell highlights noticeable

datapoints

Source : Bloomberg, SBIFM Research; NB: Coloured cell highlights noticeable

datapoints

There were a few other economies such as Switzerland, Japan and Germany, where central bankers

responded much more

swiftly and were able to tame in inflation much more rapidly despite the 1979 Oil shock (Exhibit

10).

Exhibit 10: Policy credibility mattered across countries

Source : World Bank, SBIFM Research

Source : World Bank, SBIFM Research

Box 1: What shaped inflation thinking in the 1970s?

The excerpts and quotations in this box are drawn from Edward Nelson's (2004) study, The Great

Inflation of the

Seventies: What Really Happened? Nelson compiled these statements from speeches, congressional

testimonies,

and contemporaneous newspaper archives to document how policymakers increasingly embraced

cost-push

explanations of inflation and relied on wage-price controls rather than monetary tightening

during the 1970s.

President Nixon, observing applause for Arthur Burns at Burns’ swearing-in (Feb-1970), said on

the record: “That

is a standing vote of approval, in advance, for lower interest rates and more money,” and noted,

“I have very strong views, and I expect to present them to Mr. Burns. I respect his

independence, but I hope that he independently

will conclude that my views are the right ones” (KCS, 02/01/70).

On December 4, 1969, Sylvia Porter, a financial journalist whose daily column was syndicated to

350 newspapers

in the U.S., claimed in a column entitled “Inflation: 1970- Style” that the U.S. was entering an

era of a new type of

inflation: “We are moving rapidly away from the type of inflation in which an excessive demand

for goods and

services pulls up prices (demand-pull) … We are swinging fast into an even worse type of

inflation in which

whopping wage increases will push up prices (cost-push). This type of wage-price spiral will

distort our economy

in 1970… This is the background for the emergence of the second type of inflation in our land.

(NYP, 12/04/69)”

Congressman Henry S. Reuss (D−WI) called for the President to organize a six-month price freeze

and an

agreement with labour on wages: “We should now have learned that tight money and tight fiscality

alone are not

enough” (MJ, 01/27/70).

In 1971, Chairman Burns switches to cost push view of inflation. The continuation of high

inflation beyond mid-1970 had convinced him that “the inflation we are still experiencing is no

longer due to excess demand…”.

“…monetary and fiscal tools are inadequate for dealing with sources of price inflation such as

are plaguing us

now—that is, pressures on costs arising from excessive wage increases” (December 7, 1970).

“… Despite much idle industrial capacity, commodity prices continue

to rise rapidly. And the experience of other

industrial countries, particularly Canada and the U.K., shouts warnings that even a long stretch

of high and rising

unemployment may not suffice to check the inflationary process”. (July 23, 1971, testimony, in

Burns, 1978).

1971−74: Chairman Burns would subsequently

characterize the Federal Reserve’s role in this expansionary phase

as feeling obliged to monetize the Federal government’s higher deficits, as: “the Federal

Reserve, among other

things, is the Government’s banker” (February 26, 1974, testimony, in Joint Economic Committee,

1974).

In January 1973, the six-month annualized CPI inflation rate rose to

4.4%, above the level prevailing when controls

were introduced. In August 1973, it stood at 9.5%. Chairman Burns blamed the initial rise on

“abuses of economic

power by both business firms and trade unions” (WP, 02/21/73); and in September 1973, he offered

a detailed

account of the upturn in inflation since January. There, he rejected arguments that expansionary

Fed policy in

1972 bore the blame for the rise in inflation, contending that the “severe rate of inflation

that we have experienced

in 1973 cannot responsibly be attributed to monetary management”

Money supply growth picked up again in 1975–76, well before inflation

rose in 1977. Policymakers continued to

attribute inflation to food, energy, wages and sectoral price shocks, not demand conditions.

Even falling

inflation in 1975 was explained by temporary easing in commodity prices rather than policy

restraint. Policymakers

believed output gap was deeply negative (double-digit), which validated the view that inflation

was not driven by

demand, and justified continued expansionary demand policies.

Carter administration pursued strong growth targets (e.g., ~6% real

growth). Anti-inflation measures focused on

price controls, wage guidelines, and sector interventions. Inflation control was delegated to

administrative tools,

not monetary tightening. Policymakers doubted that higher interest rates could materially

restrain demand. Wage�price guidelines were repeatedly tried (1977–78). Dollar depreciation

(1978) forced tighter monetary policy. Policy

tightening happened reluctantly and via exchange-rate concerns, not due to acceptance of

monetary causes of

inflation. Policy in 1975–78 combined expansionary demand, cost-push beliefs, and reliance on

controls, delaying

monetary tightening and setting up the late-1970s inflation resurgence.

Miller in 1978: He endorsed several aspects of the cost-push view of

inflation, suggesting that monetary policy

was becoming ineffective at restraining demand. “The public has built up some sort of antibodies

that resist the

impact of higher interest rates” (WP, 07/30/78). Although, in principle, this perspective might

mean pushing interest

rates up further than otherwise in fighting inflation, Miller said he expected interest rates to

peak soon and to begin declining in 1979, with no recession. (Source: Nelson, E. (2004), The

Great Inflation of the Seventies: What Really

Happened? Federal Reserve Bank of St. Louis Working Paper No. 2004-001)

Exhibit 11: Three episodes of stagflation

Source : Bloomberg, SBIFM

Research

Source : Bloomberg, SBIFM

Research

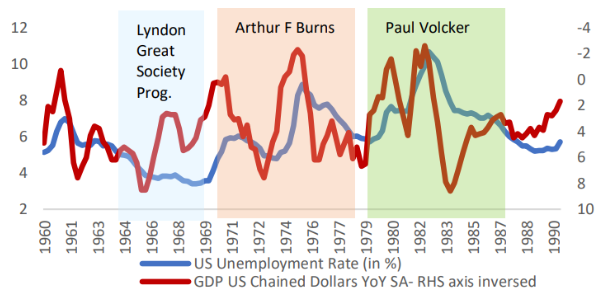

Exhibit 12: Unemployment rise in 1970s

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

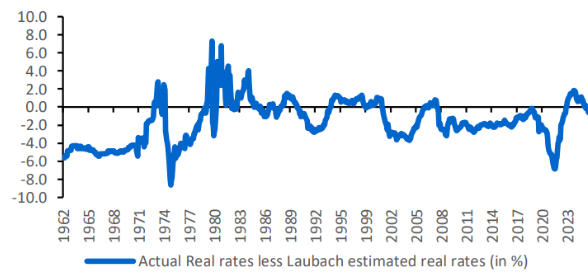

Exhibit 13: Real rates were kept much lower than

required

Source : Bloomberg, SBIFM

Research

Source : Bloomberg, SBIFM

Research

Exhibit 14: Money supply was increased to combat the

external shocks

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

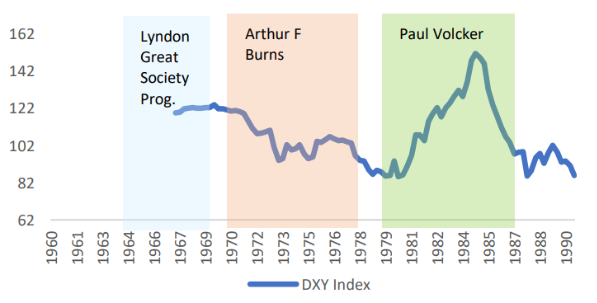

Exhibit 15: Dollar weakened throughout 1970s

Source : Bloomberg, SBIFM

Research

Source : Bloomberg, SBIFM

Research

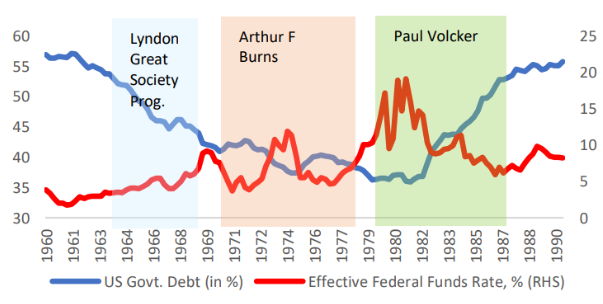

Exhibit 16: Fiscal wasn’t an issue

Source: Bloomberg, BIS, SBIFM Research

Source: Bloomberg, BIS, SBIFM Research

Inflation and the structure of the economy today

The recent cycle shows uncomfortable similarities. During the pandemic,

monetary policy was loosened

aggressively in

response to what was widely perceived as a demand shock. The shock had a significant supply-side

component. Loosening

financial conditions in such an environment increases the likelihood that rising demand will

translate into higher prices rather

than higher output.

Moreover, central banks placed significant weight on inflation expectations, if as long as

expectations remained anchored,

inflation would remain contained. History suggests otherwise. Expectations tend to adjust slowly and

may only respond after

inflation has already become entrenched.

Despite these parallels, today’s environment is not identical to the

1970s. Over the past four decades, several structural forces

have acted to suppress inflation. These include weaker labour unions, increased globalisation,

technological innovation, and

improved productivity (Exhibit 17-22).

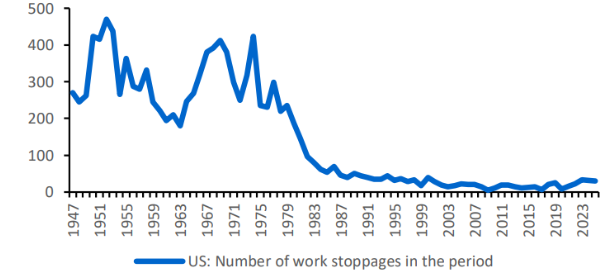

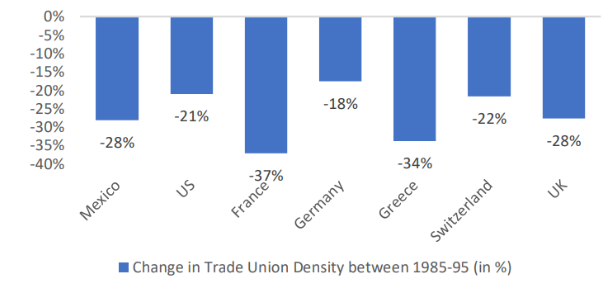

Exhibit 17: Labour rigidities amplified inflation in 1970s

Source :ILO, https://www.bls.gov/web/wkstp/annual-listing.htm, SBFIM

Research

Source :ILO, https://www.bls.gov/web/wkstp/annual-listing.htm, SBFIM

Research

Exhibit 18: Industrial relations were weak in 1960-70s

Source: ILO, SBIFM Research

Source: ILO, SBIFM Research

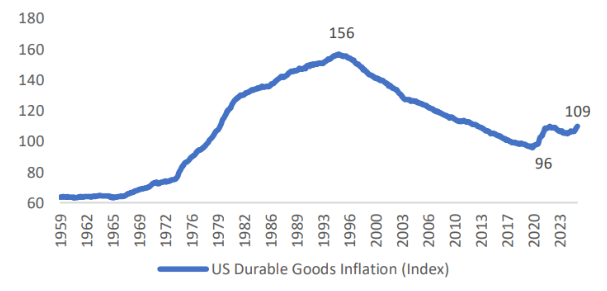

Exhibit 19: Structural disinflation in the modern era

owing to better technology

Source :Bloomberg, SBIFM Research

Source :Bloomberg, SBIFM Research

Exhibit 20: China’s role in global prices

Source: Bloomberg, CEIC, SBIFM Research

Source: Bloomberg, CEIC, SBIFM Research

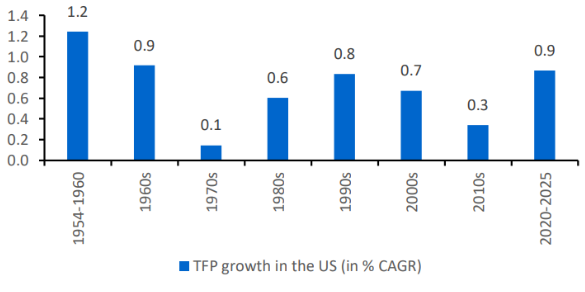

Exhibit 21: 1970s saw a significant fall in productivity.

It’s improving in the current decade

Source : St Louis Fred, US Bureau of labour statistics, SBIFM Research

Source : St Louis Fred, US Bureau of labour statistics, SBIFM Research

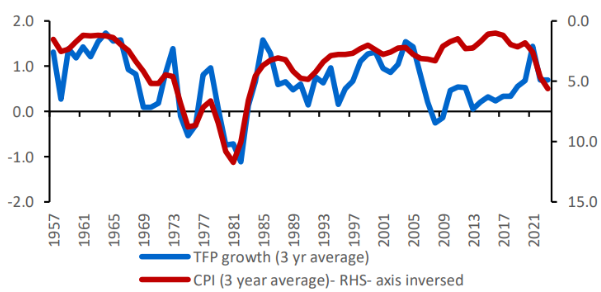

Exhibit 22: Higher productivity growth leads to

contained inflation

Source: Bloomberg, St Louis Fred, US Bureau of labour statistics, SBIFM

Research

Source: Bloomberg, St Louis Fred, US Bureau of labour statistics, SBIFM

Research

These forces helped anchor inflation during the period from the 1990s through to the pandemic.

However, some of them are

now weakening or reversing. Globalisation is giving way to geopolitical fragmentation, labour

markets are tightening, and fiscal

policy has become significantly more expansionary.

At the same time, monetary expansion during the pandemic reached unprecedented levels. While

inflation did not rise

immediately—due in part to lockdown-induced reductions in velocity—the underlying monetary impulse

remained. Once

demand normalised, the interaction between strong spending and constrained supply led to a sharp

increase in prices.

This interaction highlights a key point: inflation is not determined solely by supply or demand

conditions. It is the combination

of both, mediated through monetary policy, that ultimately determines outcomes

In practice, this structure enforces discipline but

reduces flexibility during volatile periods. Liquid funds,

for example, cannot invest beyond 91 days, while overnight

funds are restricted to one-day instruments such as TREPS.

Furthermore, equity and hybrid funds often maintain cash

balances for margin requirements related to futures

positions, and these balances cannot be freely deployed

into longer-dated CP or CD instruments.

As a result, headline liquidity metrics-such as large

volumes in the collateralized TREPS market—overstate the

amount of AUM available for CD and CP deployment (Exhibit

7). Only a subset of debt funds has both the mandate and

the risk appetite to meaningfully invest beyond overnight

instruments.

The role of credibility and expectations

The experience of the 1970s also underscores the importance of policy credibility. Once inflation

becomes entrenched, it is

extremely difficult to reverse without significant economic costs.

The turning point came with the appointment of Paul Volcker as Federal Reserve Chair in 1979. By

sharply raising interest

rates and restoring positive real rates, the Fed was able to break the back of inflation—albeit at

the cost of a deep recession.

This episode reinforced a key lesson: controlling inflation requires

decisive and credible policy action. Delayed responses only

increase the eventual cost of stabilisation.

Today, central banks have responded more quickly than in the 1970s.

Monetary policy errors were rectified rapidly from 2022

onwards. Rates have turned restrictive, and money supply growth has slowed materially. This suggests

that, in the base case,

inflation may be contained without a repeat of the extreme volatility seen in the past.

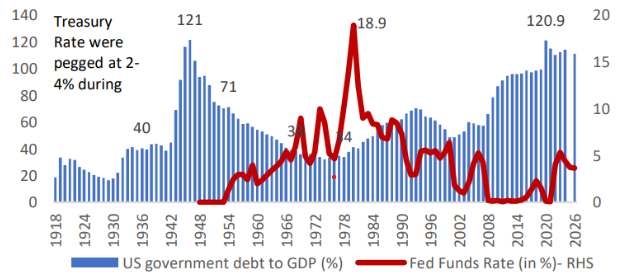

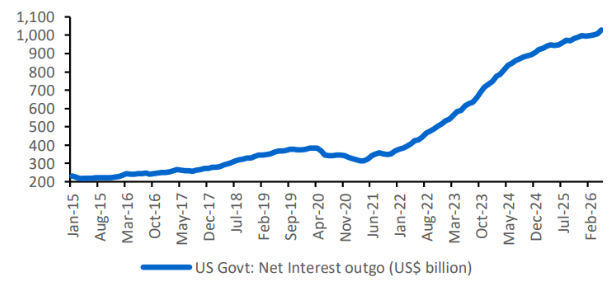

Financial repression as the key macroeconomic risk

The principal risk facing the global economy today is not a resurgence of traditional inflationary

pressures, but the possibility of

financial repression. Rising public debt burdens have materially increased fiscal vulnerabilities

(Exhibit 23), with US net interest

payments expanding from approximately $300-400 billion in 2020 to over $1trillion (Exhibit 24). This

raise concerns that fiscal

dominance could eventually constrain monetary policy, creating incentives to tolerate moderately

higher inflation as a

mechanism to reduce the real value of government debt. The Silicon Valley Bank episode demonstrated

how quickly policy

priorities can shift when financial stability concerns emerge. Although monetary policy currently

remains restrictive, with money

supply growth broadly aligned with nominal GDP growth of around 4.5%, debt sustainability pressures

continue to pose a latent

risk of policy error.

Exhibit 23: Risk of financial repression

Source :

https://www.federalreservehistory.org/essays/feds-role-during-wwii, BIS,

SBIFM Research

Source :

https://www.federalreservehistory.org/essays/feds-role-during-wwii, BIS,

SBIFM Research

Exhibit 24: Rising interest burden for US Treasury

Source: Bloomberg, SBIFM Research

Source: Bloomberg, SBIFM Research

A base case and a warning

The current environment is best understood as a transition from a low-inflation regime to one

characterised by greater

uncertainty. Structural disinflationary forces have somewhat weakened, while new risks—geopolitical

fragmentation, fiscal

expansion, and debt sustainability concerns—have emerged (Exhibit 25).

The base case remains that inflation can be contained, supported by tighter monetary policy and a

re-anchoring of expectations.

However, the primary risk lies in a gradual shift towards financial repression, where policymakers

prioritise debt management

and economic growth over price stability. Such an outcome would be more likely to produce

intermittent and volatile inflation

cycles rather than a sustained inflationary surge. In this context, real policy rates relative to

the neutral rate remain a critical

indicator of future inflation dynamics.

Exhibit 25: Then vs now – what has changed?

Source : SBIFM Research; NB: Red highlights materially adverse for inflation

outlook, amber suggest moderate inflationary pressures, green is favourable

for keeping inflation in check

Source : SBIFM Research; NB: Red highlights materially adverse for inflation

outlook, amber suggest moderate inflationary pressures, green is favourable

for keeping inflation in check

Investment implications

A regime characterised by recurring inflationary pressures would favour

real assets such as commodities, energy, and gold,

which historically outperform during periods of inflation and supply shocks (Exhibit 26).

Conversely, long-duration fixed income

assets remain vulnerable to inflation surprises and expansionary fiscal policies (Exhibit 27). The

investment environment is

therefore likely to reward active asset allocation and tactical positioning rather than reliance on

traditional long-term safe

havens.

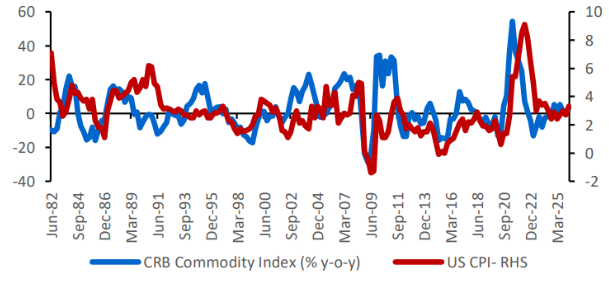

Exhibit 26: Commodities performance

Source :

Bloomberg, SBIFM Research

Source :

Bloomberg, SBIFM Research

Exhibit 27: Bond and Inflation

Source: Bloomberg, SBIFM Research

Conclusion: not a repeat, but a reminder

History does not repeat itself in precise detail. The institutional frameworks, structural

conditions, and policy tools of today differ

significantly from those of the 1970s. Yet the underlying lessons remain strikingly relevant.

Inflation is rarely the result of a single shock. It reflects broader monetary and policy dynamics.

Misdiagnosis, delayed

responses, and political interference can allow it to persist and intensify. Conversely, credible

and disciplined policy can restore

stability—but often at a cost.

The current episode should therefore be seen not as a replay of the past,

but as a reminder of the risks that arise when the

monetary anchor weakens. As long as central banks remain committed to maintaining that anchor, a

sustained inflation breakout

may be avoided. But the margin for error is thin, and vigilance remains essential.

Provided central banks maintain a credible commitment to price stability, a repeat of the

inflationary experience of the

late 1970s can likely be avoided. Nevertheless, policy misjudgement remains the single most

significant risk to the

inflation outlook.

)

)

0bf21f855da944d2a0c843c4553297d8)