Price of reigning in inflation is a recession, which seems

to be the only way out today. But the question is by when,

and how deep? And how to think about financial market

outcomes in such times.

6 coincident activity measures used by the NBER’s Business

Cycle Committee to declare recession in the US points to a

likely recession in the US by 3Q 2023 or latest by 4Q.

Leading indicators point to a significant downturn in the US

manufacturing and residential investment sector resulting in

a fall in US imports and new orders. US job market is

holding strong for now despite multiple anecdotes of

layoffs.

During inflationary periods, it's not unusual for employment

downturns to begin months, after the start of recession. We

saw that in 1973-75 and 1980 recession. Higher inflation

leads to a delayed onset of profitability loss, which in

turn delays the layoffs. Presently, corporate profit will

act as a leading indicator of wage growth and inflation

moderation.

1973 and 1980 recession saw rate hikes owing to higher

inflation and strength in job market data. Given that

inflation, corporate profits and job market data rhymes

closer to the decades of 1970s-80s, market has been

consistently trumped in pre-empting rate cuts.

Synchronized and aggressive rate hikes thus far make a case

for deeper problems in real economy ahead. The aggressive

rate hikes of 1980s to single-mindedly tame down inflation

was also made possible due to contained leverage in the

system. Things are quite different today with government

debt to GDP ~110% (vs. ~35% during 1980s). Consequently,

even as the US Fed wants to retain its inflation fighting

credibility, the issue of financial stability (emanating

from high leverage) will make it harder going ahead.

Aggressive tightening thus far and concerns on financial

stability implies slower growth going ahead and then key is

to figure out how does market behave during growth

corrections. Equity market starts to correct prior to

recession onset but bottoms out even as we are into the

recession. During 1973, 2001 and 2008 recession, S&P fell by

~50%. On other occasions, there has been ~20% corrections

(1981, 1990 and 2020 recession). Currently, S&P has fallen

17% from its peak.

The template for fixed income assets were very different

during 1970s-80s, compared to last three decades when

duration assets start to perform at mature stage of rate

cycle.

2022 was one of the worst years for combined returns of

stocks and bonds market in the US. In 2023, equity market

prospects is still grim unless we see a significant dovish

tilt by the US Fed and greater clarity on depth and breadth

of recession. Outlook for duration assets is improving at

the margin. That said, longevity of duration rally can be

challenged unless inflation is brought under complete

control.

Almost since the start of Fed tightening in the first

quarter of 2022, the most frequently asked question about

the global economy has been whether the FOMC’s fight to tame

inflation inevitably means the US economy is heading for

recession. Price of reigning in inflation is a recession,

which seems to be the only way out today. But the question

is by when, and how deep? And how to think about financial

market outcomes in such times.

Dating committee referred data hints at US recession by end

2023.

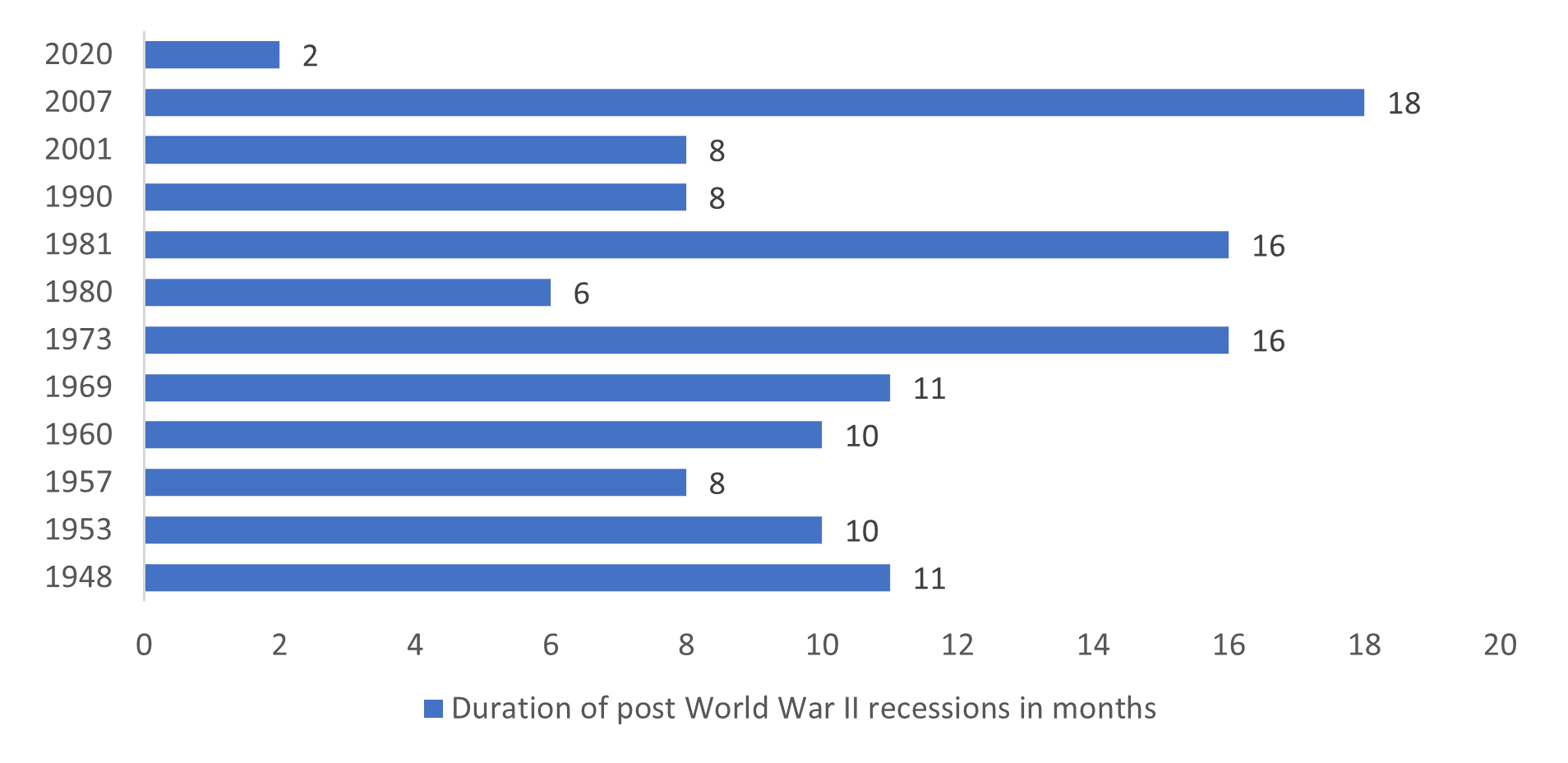

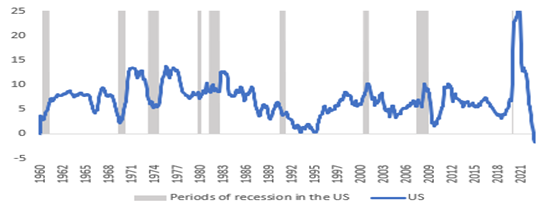

The US has seen 12 recessions post World War with 2008 GFC

being the longest and 2020 COVID being the shortest (Chart

1). The country has a separate organization, National Bureau

of Economic Research (NBER) which declares recession and it

may not necessarily coincide with the technical definition

of recession. NBER determines recession based on six

coincident monthly indicators listed below.

-

FRED real personal income less transfers

-

FRED nonfarm payrolls

-

FRED real personal consumption expenditures

-

FRED real manufacturing and trade sales

-

FRED household employment

-

FRED index of industrial production

Chart 1: US has seen 12 recessions since World War II,

typically lasting around three quarters

Source: NBER, SBIMF Research

Source: NBER, SBIMF Research

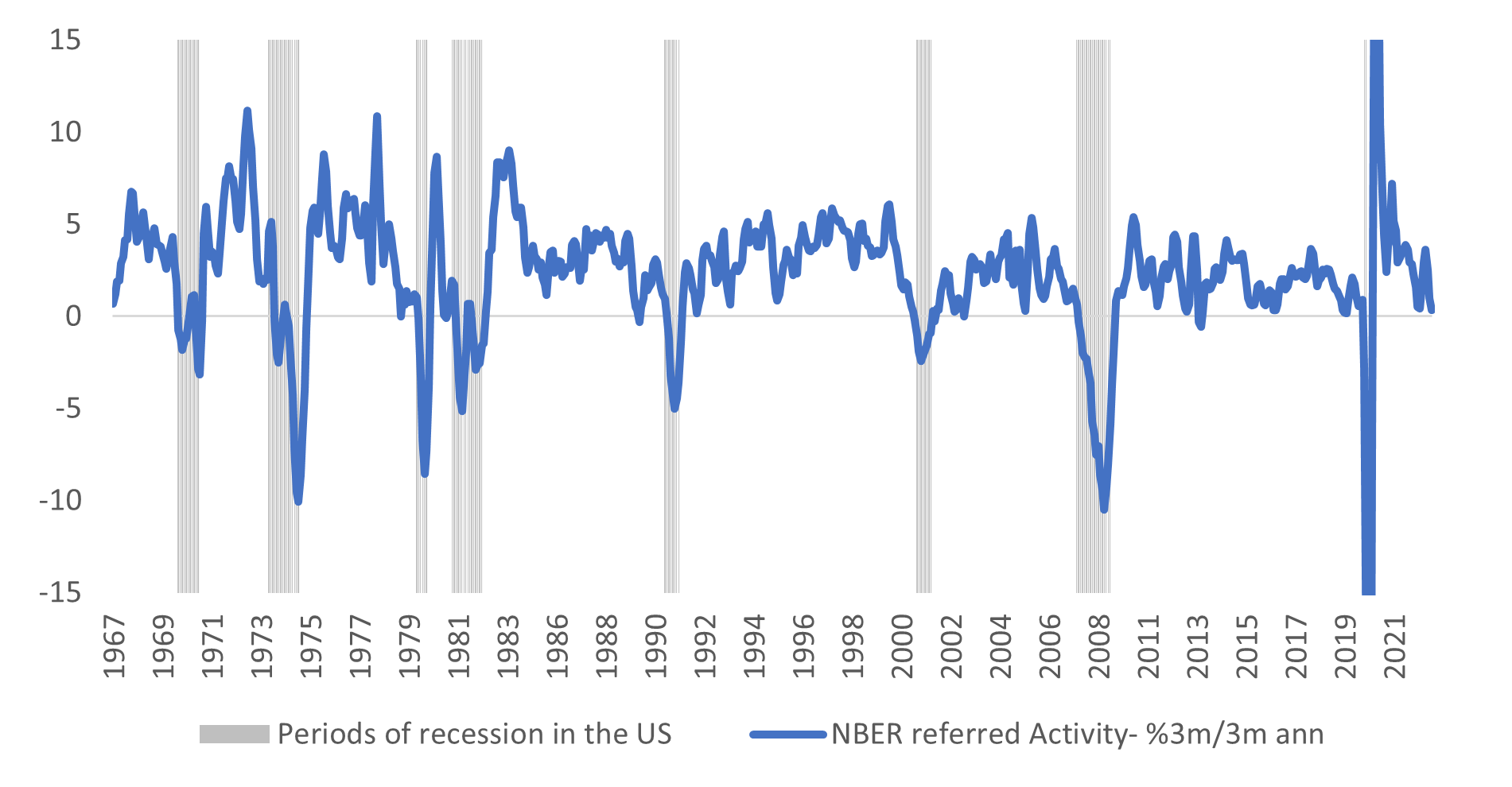

We looked at a simple average of %3m/3m annualized growth

rate for these six indicators. At an aggregate, it points to

a marginal expansion (0.4% 3m/3m ann. in Jan’23).

Historically, US has been declared into recession when the

aggregate of these activity indicators dips into

contraction. As of Jan’23, industrial activity shows

sharpest decline (-4.6% 3m/3m ann.), manufacturing and trade

sales are weak (0 on 3m/3m ann.). While on the other hand,

real income and non-farm payroll still holds up (2.1% and

2.5% respectively). Trend in these indicators point to a

likely recession in the US by 3Q 2023 or latest by 4Q.

Further, it is not necessary for all indicators to be in

negative for NBER to call out a recession in the US (1960,

1973, 1981 being a case in point).

A typical US recession starts with roll down in business

activity followed by job market slowdown

Industrial production and business sales are typically the

first one to start weakening in any recession followed by

employment (NFP and household employment). Household income

and employment roll over few months later, but may not

necessarily weaken as much (case of 1981, 2001). In 2001 –

in what was the mildest US recession ever (real GDP barely

declined) – employment fell in the first month of the

recession, because of a drop in manufacturing jobs amidst an

industrial recession. At the other extreme, during the most

severe post-war recession (until COVID) in 2008, all the key

components started to contract in Q1 2008, with consumption

lagging by just a couple of months.

Chart 2: US dips to recession when the aggregate of these

activity indicators posts negative print

Source: FRED, SBIMF Research; NB: Simple average of %

3m/3m ann of 6 coincident activity measures used by the

NBER’s Business Cycle Committee

Source: FRED, SBIMF Research; NB: Simple average of %

3m/3m ann of 6 coincident activity measures used by the

NBER’s Business Cycle Committee

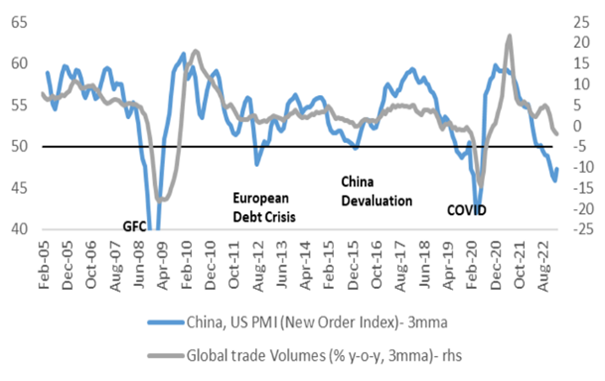

US is already amidst industrial recession with rapid

moderation in global trade

For the past year, the US has been undergoing what might be

described as step-by-step suppression of demand. Leading

indicators are pointing to a downturn in the US

manufacturing and construction (residential investment)

sector resulting in a fall in US imports and new orders. The

latest leg of the evolving slowdown is the one that the rest

of the world is feeling- i.e. the demand impact of receding

US imports.

But, with employment growth still strong, it is quite unlike

the recessions of recent decades.

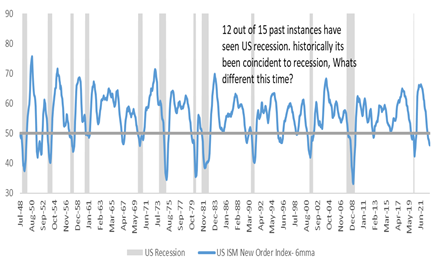

Chart 3: US ISM New Order in contraction since Sep’22

Chart 4: Global order inflows and trade volumes fall

Source: Bloomberg, SBIMF Research

Source: Bloomberg, SBIMF Research

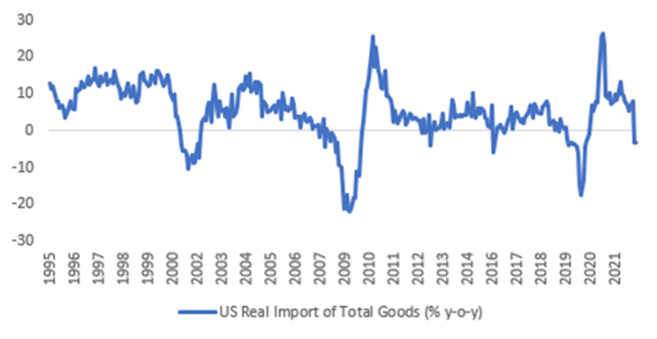

Chart 5: US real import growth contracts

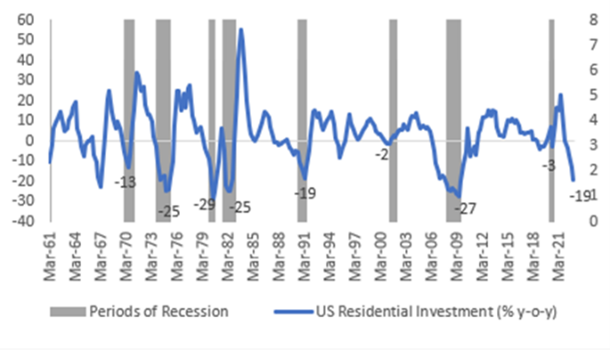

Chart 6: US Residential investment deeply negative

Source: Bloomberg, SBIMF Research

Source: Bloomberg, SBIMF Research

Strength in the US job market is the biggest issue today.

Even as there are anecdotes of layoff, non-farm Payroll has

been exceptionally strong. Unemployment rate at 3.4% is at

record low. There are 1.9 jobs in the market today for every

one person looking for job which keeps the wage growth

elevated and inflation stickier than expected.

Illusion of Money: track corporate profits to understand job

market

Typically, on most occasions of past recessions, the

incremental hiring activity at least starts to flatten

out/contract five to six months prior to recession. During

2008 GFC, negativity in jobs led the GDP growth negativity

by 6 months. But during inflationary periods, it's not

unusual for employment downturns to begin months, after the

start of recession, i.e. we can be inside a recession and

still have jobs growth. We saw that in 1973-75 and 1980

recession. This can be best described as illusion of money

during inflationary times. Higher inflation leads to a

delayed onset of profitability loss, which in turn delays

the layoffs. Thus, in today’s time too, corporate profit

will act as a leading indicator of job loss.

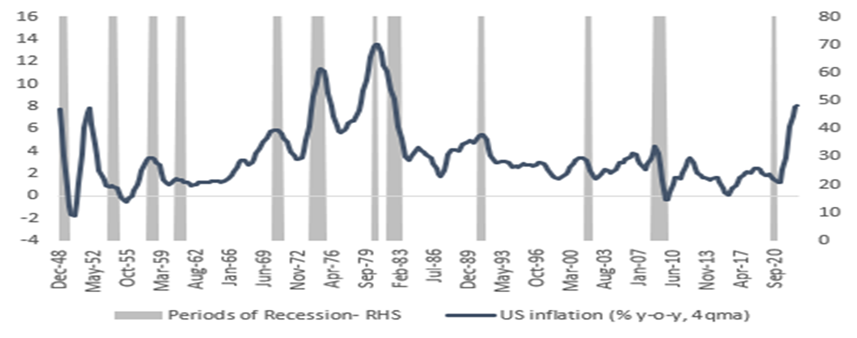

Chart 7: History of US inflation and the recession

Source: Bloomberg, SBIMF Research

Source: Bloomberg, SBIMF Research

Chart 8: During 1973-75 and 1980, healthy corporate

profits kept the job market data strong

Source: Bloomberg, SBIMF Research

Source: Bloomberg, SBIMF Research

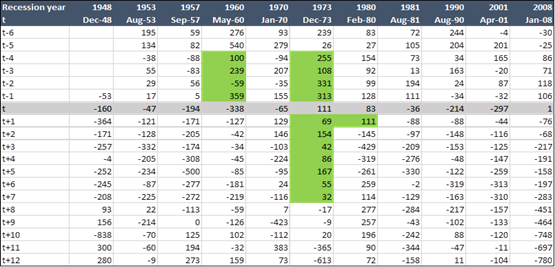

Table 1: 1973 and 1980 saw jobs growth even into recession

Source: Bloomberg, SBIMF Research; NB: t refers to the

month of recession onset

Source: Bloomberg, SBIMF Research; NB: t refers to the

month of recession onset

Genuine inflation is nothing more than excessive money

creation chasing too few goods.

While there have been notable supply side improvements,

demand side of the economy remains strong supported by

healthy wage growth. Along with that, the impact of

structural factors relating to geopolitical factors and

energy transition costs add considerable uncertainty.

Policy makers expected that 1970s recession would tame in

inflation. But that did not happen as money supply growth

was strong. 1970s had an excessive money supply growth which

has been curtailed this time. Monetary tightening will

eventually drive cyclical disinflation.

Chart 9: Money supply growth were elevated during 1970s

feeding into stagflation

Source: Bloomberg, SBIMF Research

Source: Bloomberg, SBIMF Research

As monetary policy works with a lag, we could see its effect

in coming months on both growth and inflation. And with

growth likely slowing across much of the world, commodities

will not be the source of inflation they were over 2021 and

2022 (though they may not see a material dip down either).

The cyclical inflation will come down but there are

structural changes in economy. Global trade has slowed post

GFC. Constrained energy supply, falling productivity and

geopolitics seems most credible threat to medium-term

inflation. Consequently, while CPI could fall owing to

significant tightening- we do not know if it could rise

again as the monetary breaks go loose.

US Fed has been single-mindedly focussed on inflation to the

extent of engineering recession but such aggressive hikes

cannot be without no broken bones especially when leverage

is high.

In the past three decades, Federal Reserve that has

typically cut interest rates before the recession has even

begun. However, 1973 and 1980 recession saw rate hikes owing

to higher inflation and strength in job market data. Given

that inflation, corporate profits and job market data rhymes

closer to the decades of 1970s-80s, market has been

consistently trumped in pre-empting rate cuts. US Fed has

hiked rates by 475bps in the current cycle, guides for one

more and then a long pause in 2023.

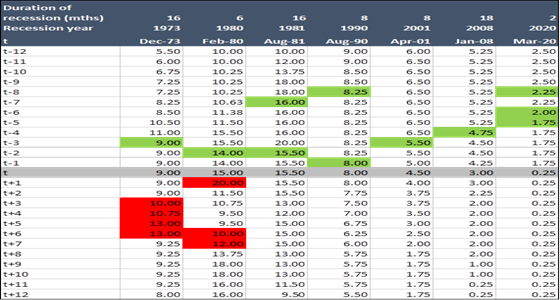

Table 2: 1973 and 1980 recession saw rate hikes owing to

higher inflation

Source: Bloomberg, SBIMF Research; NB: t refers to the

month of recession onset

Source: Bloomberg, SBIMF Research; NB: t refers to the

month of recession onset

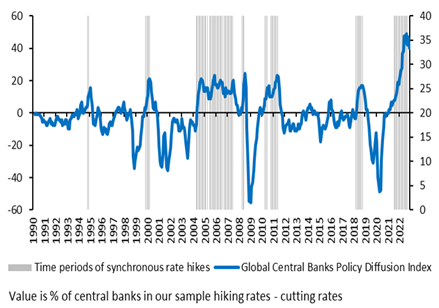

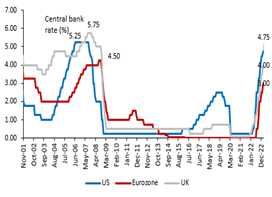

We are witnessing synchronized and aggressive global

monetary tightening at a time when industrial recession has

already begun. We do not know how severe this recession is

going to be. But the kind of aggression in rate hikes makes

a case for more severe than for being it mild.

Chart 10: Synchronized policy tightening

Chart 11: And too high too soon.

Source: Bloomberg, SBIMF Research; NB: Global Central Bank

policy diffusion index is based on sample of 30 countries

Source: Bloomberg, SBIMF Research; NB: Global Central Bank

policy diffusion index is based on sample of 30 countries

Leverage if the biggest problem today. The aggressive rate

hikes of 1980s to single-mindedly tame down inflation was

also made possible due to contained leverage in the system.

US had successively managed to bring down its post war debt

(from 95% of GDP in 1947 to 35% of GDP in 1980). Well,

things are quite different today.

Government debt to GDP stands at 110%. Even as the real

economy impact may be delayed, recent events in the US and

European banking space confirmed, in case there was ever any

doubt, that the fastest and most aggressive tightening cycle

in four decades is having an impact. The entire last decade

was built on era of low inflation, near zero rates and

large-scale asset purchases. Today, financial institutions

have found themselves inadequately hedged against interest

rate risks. Further bouts of turmoil cannot be ruled out.

US Fed today: Damned if you do, Damned if you don’t.

Banking sector concerns led markets to price an abrupt end

to the hiking cycle and a substantial probability of policy

rate cuts. Well, that did not happen. Fed Funds rate was

hiked by another 25bps in Mar’23 meeting and the dot plot

remained unchanged implying one more hike and then a long

pause in 2023

But market wants cuts- fast and deep. Inflation and

employment backdrop is too strong for the US Fed to go all

out in the support of financial stability. Either of the two

thing has to happen for market expectations to materialize.

If the earning recession that we spoke of commence and US

start losing jobs or inflation solves for itself in next

couple of months- that would help the Fed to lend an extra

support on financial stability. Or another possible outcome

is that more of Silicon Valley types issue spring up,

leading Fed to prioritize financial stability over

inflation.

To certain extent, the current banking sector episode in the

US will translate into tighter regulations and profitability

compression for banks, implying tighter credit conditions.

In a fractional reserve banking system, this is the

transmission mechanism slowing growth. But that aside, this

financial turmoil will make it difficult for the Fed to

fight inflation as hard as they desired. And that in turn

means that market volatility will continue as investors keep

betting on assets that have higher beta to dovish tilt and

assets that do not.

How does US equity market behave during their recessions?

Both aggressive tightening thus far and concerns on

financial stability implies slower growth going ahead and

then key is to figure out how does market behave (we study

equity and fixed income here) during growth corrections.

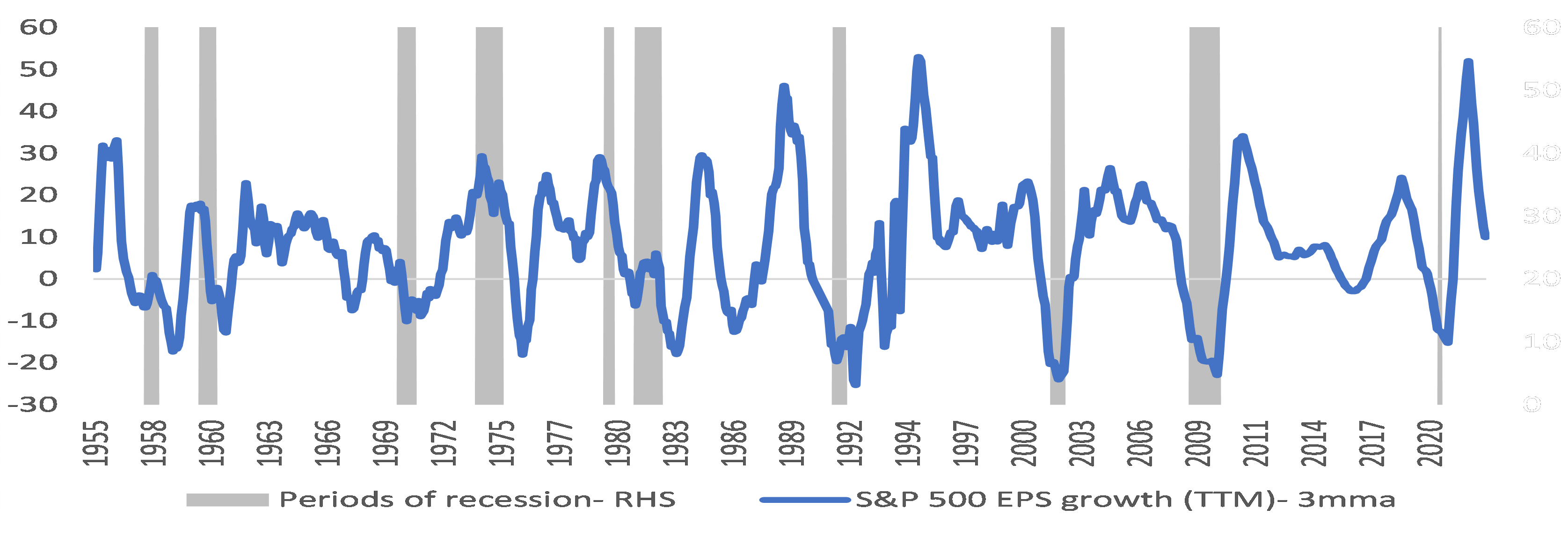

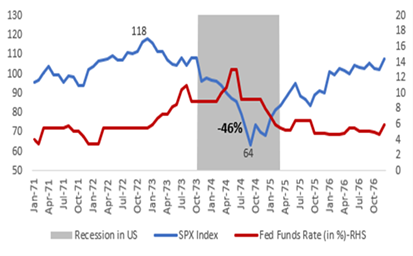

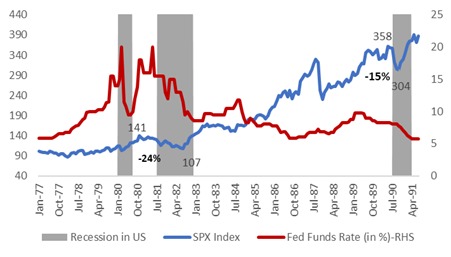

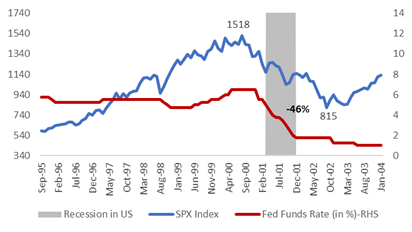

We studied past recession in the US and figured out that

equity market starts to correct prior to recession onset but

bottoms out even as we are into the recession- with few

exceptions. One such exception is the equity market bull run

of 1980s. During 1980s, we had three episodes of recession

within a decade. There were small market corrections- but

not meaningful given the extent of rally we saw during that

period. One plausible reason could be massive decline in Fed

Funds rate during the decade which could have led to equity

valuation re-rating. Fed Funds rate fell from 20% to settle

at 5% by 1990s. On the other hand, during 1973, 2001 and

2008 recession, S&P fell by ~50%. On other occasions, there

has been ~20% corrections (1981, 1990 and 2020 recession).

Currently, S&P has fallen 17% from its peak.

Thus, if history is any guide, there are more pains left and

perhaps equity market should bottom out by end 2023.

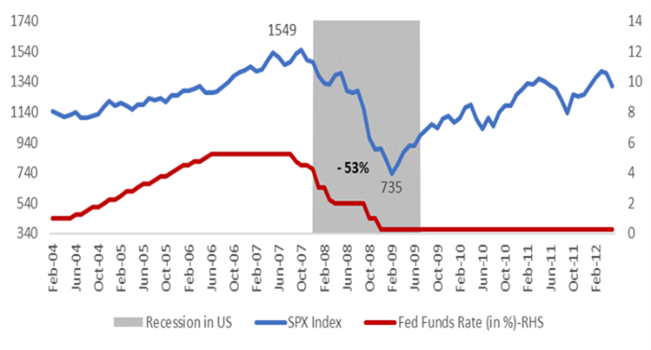

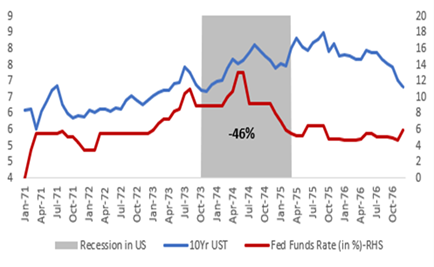

Chart 12: 1973 Recession- market corrects 46%

Chart 13: 1980, 1981 and 1990 Recession

Chart 14: 2001 recession

Chart 15: 2008 Recession

Source: Bloomberg, SBIMF Research

Source: Bloomberg, SBIMF Research

When does Duration start to perform?

If one were to look at last two decades, the answer is very

simple. Duration starts to perform at mature stage of rate

hiking cycle. However, the high inflationary periods of

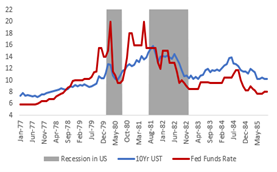

1970-80s were very different. 10-year UST rose into 1973 and

1980 recession. That could perhaps be explained by high

inflation leading market to doubt the longevity of rate

cuts.

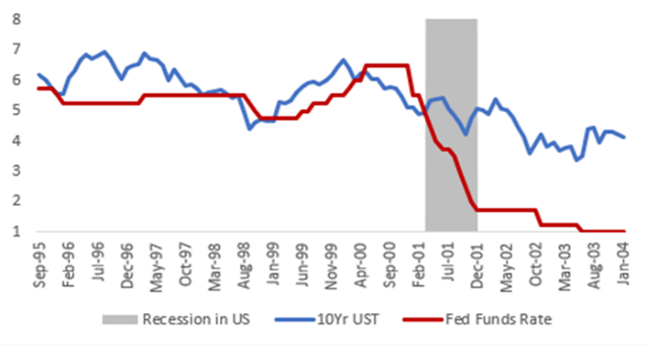

Chart 16: 2001 Recession and 10Yr UST

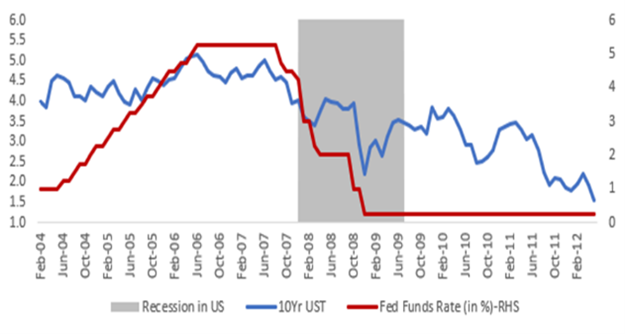

Chart 17: 2008 Recession and 10Yr UST

Chart 18: 1973 recession and 10Yr UST

Chart 19: 1980s recession and 10Yr UST

Source: Bloomberg, SBIMF Research

Source: Bloomberg, SBIMF Research

On top of that, another angle is the financial stability

concerns. 2008 GFC crisis was followed by sharp rate cuts.

But in 1980s financial stability concerns had interrupted

the hiking cycles but did not end them.

Mapping this history in the current context, sharp monetary

tightening in last one year should drive cyclical

disinflation- though one could argue that 2% inflation

target may still be far-fetched. On top of that, the issues

of financial stability could provide a breather to rate

hikes. But like we said, we do not know as yet whether

market today is mimicking the past three decades a long

period rally in fixed income assets or 1970-mid 80s where

the rally is short-lived and frequently punctuated with

reversal in rate cycles.

2022 was one of the worst years for combined returns of

stocks and bonds market in the US. In 2023, equity market

prospects is still grim unless we see a significant dovish

tilt by the US Fed and greater clarity on depth and

breadth of recession. Outlook for duration assets is

improving at the margin. That said, longevity of duration

rally can be challenged unless inflation is brought under

complete control.

This presentation is for information purposes only and is

not an offer to sell or a solicitation to buy any mutual

fund units/securities. The views expressed herein are based

on the basis of internal data, publicly available

information & other sources believed to be reliable. Any

calculations made are approximations meant as guidelines

only, which need to be confirmed before relying on them.

These views alone are not sufficient and should not be used

for the development or implementation of an investment

strategy. It should not be construed as investment advice to

any party. All opinions and estimates included here

constitute our view as of this date and are subject to

change without notice. Neither SBI Funds Management Limited,

SBI Mutual Fund nor any person connected with it, accepts

any liability arising from the use of this information. The

recipient of this material should rely on their

investigations and take their own professional advice.

)

d7a82bd424794b57a015914cd7b8baab)

)

)