Stay invested for the long term

Short-term rallies are par for the course in the equity

market. Don’t let them scare you. Stay focused and invested

for the long term as it enhances the chances of optimising

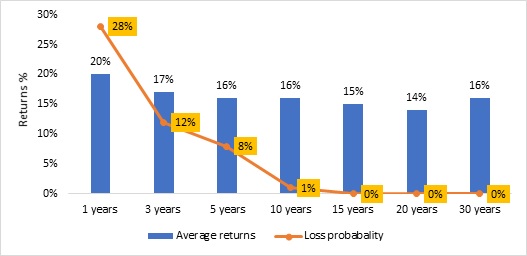

returns and reducing risks. For instance, the S&P BSE Sensex

has returned average 20% for the one-year daily rolling

return period since its inception in 1979 till August 31,

2019. However, this average includes periods of loss; the

loss probability (count of negative returns / total number

of returns) is as high as 28% in this short-holding period.

However, as the investment period expands, we see reduction

in probability of loss in a holding period of 15-20-year

rolling basis. Hence the investor shall always focus on the

long term investment in order to aim to generate returns.

Increasing investment horizon results in return

optimisation

Source: BSE

Increasing investment horizon results in return

optimisation

Source: BSE

Notes: Past performance may or may not be sustained

in future. Daily rolling returns of S&P BSE Sensex since

inception (1979) considered across various periods. Data

for the period ended August 31, 2019.

Opt for systematic investments

Investors would be better off in the long run by investing

systematically (systematic investment plan or SIP) to derive

best benefits from the markets. In basic parlance, a SIP is

similar to a recurring bank deposit; investors contribute a

fixed sum of money at regular intervals. SIP negates the

risk of market timing, averages the cost per unit and adds

discipline to investments over the long term. Multiple

benefits have enhanced the popularity of SIP among retail

investors in recent years, as is evident from SIP inflows of

Rs 2.37 lakh crore from April 2016 to July 2019.

CRISIL Research’s analysis reveals that

SIP investments

have generally done better than lump sum returns in most

bear phases. For instance, during the sub-prime crisis

(January 2008 to March 2009), when the global markets

toppled ~45%, SIP investors’ returns were negative, so also

during the European crisis i.e. during January 2011 to June

2013 (SIP returns of 5.60% were more than lump sum returns

of -2.21%). During the bull run, there have been instances

of a sharp bounce-back after the sub-prime crisis (April

2009-December 2010) - lump sum returns were more attractive

at 51.58% than 28.76% SIP returns. However, in the post

European crisis during July 2013-February 2015, SIPs returns

(31.51%) benefitted more than lump sum returns (27.60%).

The clinching deal for SIPs came in the cumulative period

since 2008 till August 2019 when point-to-point CAGR returns

were just 5.36% versus XIRR returns of 9.76% through the

systematic route, thus showcasing the dividend of

disciplined and regular investments by investors. Investors

can optimise SIPs over the long run, helping reduce risks

from volatility in the underlying market and aim for shoring

up returns.

Investors with lump sum can invest via STP

Investors with lump sum money and wanting to invest in the

equity market, while not risking timing the market, can go

for systematic transfer plan (STP). In this, investors

invest their money in a

individual's risk profile, mostly liquid funds, and transfer money from that fund on

a periodic frequency to an equity fund of their choice. By

doing so, they may not only generate money from their

investment in the debt fund, but also aim to reduce the risk

of timing the equity market, rather investing systematically

in an equity fund. Debt funds can also be an option for the

investors to park money in the short to medium term. For

short-term goals and low risk appetite, investors can

consider investing in debt funds such as overnight, liquid,

ultra short-term, and money market funds.

Summing up

An equity investor cannot escape market volatility. Hence,

it is best to avoid the herd mentality and be rational.

Patience is the panacea. One of the best ways to overcome

influence of the crowd is to focus on an investment strategy

which is in line with individual financial goals and risk

profile.

Investors shall always refer to the Scheme Information

Document and Key Information Memorandum of the schemes

carefully to understand the investment objective and

associated risk factors of the scheme before investing.

Disclaimer:

Any comparison mentioned in this material is for general

information only and not intended to be relied upon as

investment advice and is not a recommendation, offer or

solicitation to buy or sell any securities or to adopt any

investment strategy. Information and content herein have

been provided by CRISIL Research, a Division of CRISIL

Limited, and is to be read from an investment awareness and

education perspective only. Recipient are advised to seek

independent professional advice before making any

investments. The views / content expressed herein do not

constitute the opinions of SBI Mutual Fund or recommendation

of any course of action to be followed by the reader. SBI

Mutual Fund / SBI Funds Management Private Limited is not

guaranteeing or promising or forecasting any returns.

-1)

-1)

-197095f6910be4204af609b63a23bef97)

)