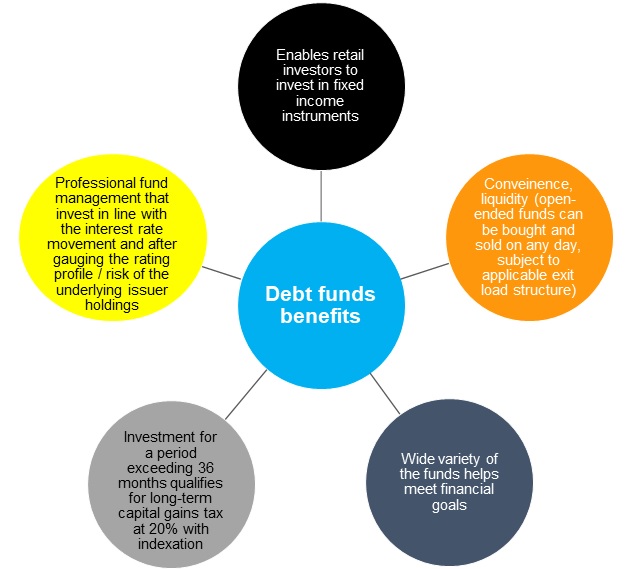

Debt funds – reasons for the rise in popularity

Debt funds, unlike traditional bank deposits, provide investors with

the opportunity to generate market-linked returns by

professional investment. While fixed deposits generally aim

to provide guaranteed returns and safety to capital, subject

to the applicable terms and conditions1 , debt mutual funds, at a slightly higher risk, provide investors with an

opportunity to invest across the debt spectrum based on

their risk-return profile and investment horizon.

Further, on the tax front, interest from bank deposits is

taxed as per the applicable tax slab of the investor, while

for debt mutual funds, investment for a period of less than

or equal to three years is subjected to short-term capital

gains tax (STCG) and hence is taxed as per applicable tax

slabs, and investment for a holding period of more than

three years, is subject to long term capital gain tax (LTCG)

and is taxed at 20% with indexation. The latter is quite

beneficial for investors with more than three years of

investment horizon, as it reduces the tax incidence

1Subject to maximum of Rs. 1 lakh by the Deposit

Insurance and Credit Guarantee Corporation (DICGC), in terms

of applicable regulations and other conditions.

A plethora of positives

Options within debt funds to meet all short- to medium-term

goals

Additionally, debt funds offer a wide variety of choice;

there is something for every investor profile. Choice of

funds is based on personal criteria (investment horizon,

risk profile and return expectations), credit profile and

the underlying interest rate scenario.

For short-term goals and low risk appetite

Investors with a low risk appetite aiming to build an

emergency fund or having short-term goals, such as

children’s tuition fees and settlement of one-time bills,

can invest in liquid funds instead of a savings account as

the former has the potential to generate better returns at

reasonable liquidity.

Investors with a low risk-bearing capacity and short-term

horizon (from a day to a week) can choose overnight funds.

Investors with a slightly higher risk-bearing capacity can

consider investing in ultra short-term funds and low

duration funds. Note, short duration funds typically do

well in a rising interest rate scenario and they are less

sensitive to interest rate changes.

For medium- to long-term goals and ability to bear

moderate to high risk

There are short to medium duration funds with an

investment horizon of 1 to 4 years. Further for investors

with a high-risk appetite intending to invest for a medium

to long term, debt funds like gilt funds, dynamic and long

duration funds etc. with investment horizon of 4 years and

above are available.

Meanwhile, investors with the ability to take risk or the

affinity to invest in corporate bonds can look at credit

opportunity and corporate bond funds / banking and PSU funds. A credit risk fund invests minimum 65% of its

assets in corporate bonds which shall not be highest rated

instruments, while a corporate bond fund invests minimum

80% in highest rated corporate bonds.

addition, investors can consider

fixed monthly plans (FMPs)

, which resonate with bank deposits. FMPs follow a

buy-and-hold strategy which can help investors lock-in

higher yields for the entire investment period. FMPs are

close-ended debt funds with varying maturity tenures

starting from three months to five years. Investors can

only invest in or enter at the time of a new fund offer

(NFO) period. Investors wishing to exit may do so, through

the stock exchange where the FMP is listed. Redemption of

the units of the FMPs is not allowed prior to the maturity

of FMP. FMPs can generate higher tax-adjusted returns

because of the benefit of indexation (adjusting gains

after considering inflation) for a holding period of more

than three years.

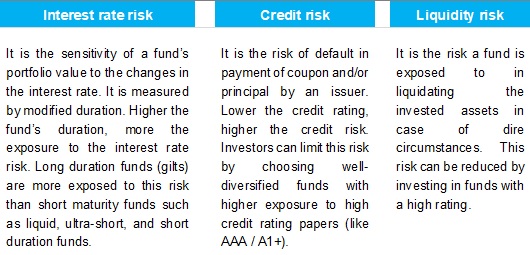

Evaluate underlying risk factors before debt funds

investment

While debt funds offer a good opportunity to investors with

a low risk profile, they do come with some risks. That

notwithstanding, investors should evaluate all schemes based

on the underlying risk factors and map them onto their

risk-return profile and investment horizon.

Chart: Important risks related to debt funds

Apart from the above, certain other risks to which the

debt mutual funds are exposed to are reinvestment risk,

regulatory risk, currency risks, risk associate with

investment in derivatives, foreign instruments, etc,

depending on the investment objective and the strategy of

the fund. Investors shall always refer to the Scheme

Information Document and Key Information Memorandum

carefully to understand the detailed risk factors

associated with the particular mutual fund schemes.

Apart from the above, certain other risks to which the

debt mutual funds are exposed to are reinvestment risk,

regulatory risk, currency risks, risk associate with

investment in derivatives, foreign instruments, etc,

depending on the investment objective and the strategy of

the fund. Investors shall always refer to the Scheme

Information Document and Key Information Memorandum

carefully to understand the detailed risk factors

associated with the particular mutual fund schemes.

Disclaimer:

Any comparison mentioned in this material is for general

information only and not intended to be relied upon as

investment advice and is not a recommendation, offer or

solicitation to buy or sell any securities or to adopt any

investment strategy. Information and content herein has been

provided by CRISIL Research, a Division of CRISIL Limited,

and is to be read from an investment awareness and education

perspective only. Recipient are advised to seek independent

professional advice before making any investments. The views

/ content expressed herein do not constitute the opinions of

SBI Mutual Fund or recommendation of any course of action to

be followed by the reader. SBI Mutual Fund / SBI Funds

Management Private Limited is not guaranteeing or promising

or forecasting any returns.

In view of the individual nature of the financial or tax

consequences, each investor is advised to consult his/her

own financial/tax consultant with respect to specific tax

implications arising out of their participation in

investments. The tax rates are as per current tax laws and

are subject to change.

Mutual Fund investments are subject to market risks, read

all scheme related documents carefully.

)

)

-197095f6910be4204af609b63a23bef97)

)