Key Considerations While Planning Investments for Your Child

● Start early: Begin investing as soon as possible to benefit from the potential of compounding

● Define clear goals: Choose investments based on well-defined short-term and long-term financial objectives

● Align with time horizon: Select an investment approach that matches your child’s age and the time available to achieve each goal

Funds Designed to Cater to Your Child’s Financial Needs

Children’s mutual funds, designed to address a child’s financial needs, fall under solution-oriented schemes. These funds are structured to support long-term goals such as education and key life milestones. They typically come with a lock-in period of at least 5 years or until the child attains 18 years of age (whichever is earlier), thereby encouraging a disciplined and long-term investment approach.

Our Offering

SBI Children’s Fund is a solution-oriented mutual fund scheme designed to help you build a financial foundation for your child’s aspirations, such as education and marriage. It follows a hybrid approach by investing in a diversified mix of equity and debt, aiming to balance growth potential with relative stability. This balanced approach aims to support long-term wealth creation while helping manage market volatility, an important factor when building a sufficient corpus over time.

It offers two plans: Investment and Savings Plan both are actively managed with difference in portfolio allocation:

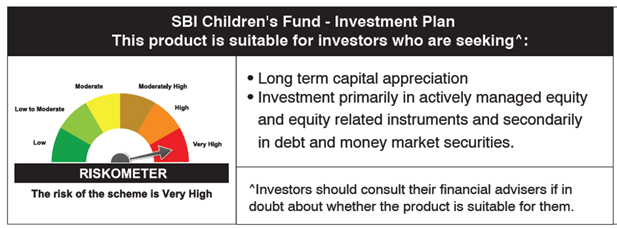

1. SBI Magnum Children's Benefit Fund- Investment Plan

This is an equity-oriented scheme that invests 65%–100% of its assets in equities and follows a multicap strategy, allowing flexibility across market capitalizations. The portfolio is built using a mix of high-conviction ideas, exposure to mid- and small-cap stocks, and macroeconomic views. It also includes high-quality debt instruments and money market securities, with optional allocations up to 20% in gold and up to 35% in foreign securities, based on the fund manager’s discretion.

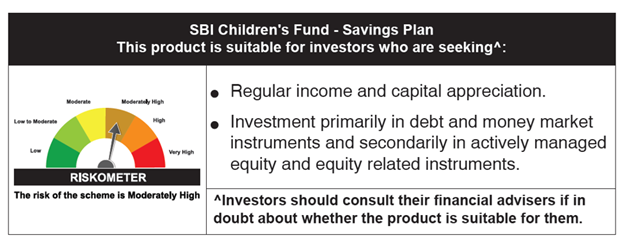

2. SBI Magnum Children's Benefit Fund- Savings Plan

This is a debt-oriented scheme that invests 75%–100% of its assets in debt instruments, with a focus on high-quality securities such as AAA-rated and sovereign papers. It actively manages both the equity component and the debt duration, while selectively including well-researched lower-rated papers to balance yield and safety. Additionally, the fund may allocate up to 25% in foreign securities at the fund manager’s discretion.

Features of SBI Children’s Fund

● Flexible investment options: Start with a SIP of ₹500 or a lump sum of ₹5,000

● Lock-in period: Encourages discipline and long-term growth (having a lock-in for at least 5 years or till the child attains age of maturity (whichever is earlier)

● Tailored plans: Investment and savings plan for children based on different asset allocation strategies, equity oriented or debt oriented as per risk appetite and investment horizon.

● Expert management: Handled by experienced fund managers

● Goal-based investing: Designed to support education and other aspirations

Investors are advised to refer to the Scheme Information Document (SID), Key Information Memorandum (KIM), factsheet, and other scheme-related documents for complete details. For more information, visit www.sbimf.com.

Is it Better to Invest via a Lump Sum or a Systematic Investment Plan (SIP)?

The choice between a lump sum investment and a Systematic Investment Plan (SIP) depends on your financial situation and personal preferences.

Some investors prefer to invest a lump sum when they have surplus funds available—such as an annual bonus or windfall gain. Others prefer a SIP approach, where a fixed amount is invested regularly, making it easier to build discipline as part of a monthly budget. There are also investors who opt for periodic investments aligned with their cash flows, such as quarterly or half-yearly contributions.

Whichever approach you choose, investing regularly can help you benefit from rupee cost averaging. This means that when markets are lower, your fixed investment amount buys more units, and when markets rise, the value of your existing investments increases—helping smooth out the impact of market fluctuations over time.

Few Mistakes to Avoid When Investing for Your Child

● Starting too late: Every year of delay reduces the time available for compounding, which can significantly impact on the final corpus. Starting early allows your investments to grow more efficiently over time.

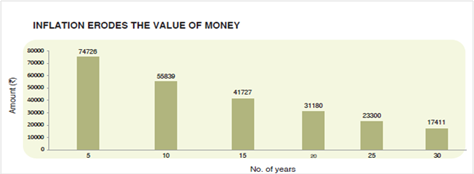

● Ignoring inflation: Setting a goal based on today’s costs can lead to a shortfall in the future. For instance, a college education costing ₹20 lakh today may require a much higher amount over the next 10–15 years. It is important to factor in realistic inflation while planning.

● Inconsistent investing or frequent withdrawals: Irregular contributions or withdrawing investments midway can disrupt the compounding process. Children’s funds, with their lock-in feature, help encourage discipline and reduce the temptation to pause or withdraw prematurely.

● Choosing the wrong investment for the time horizon: Investing too aggressively for short-term goals or being too conservative for long-term goals can impact outcomes. Aligning asset allocation with the investment horizon is key.

● Not reviewing your portfolio: Markets and personal goals evolve over time. Regular reviews help ensure your investments remain aligned with your child’s financial needs.

● Withdrawing without a clear purpose: Using funds meant for your child’s future for unrelated expenses can derail long-term goals. A dedicated investment plan should remain focused on its intended purpose.

Avoiding these common pitfalls can keep your plan on track—what truly makes the difference, however, is taking the first step at the right time. Investing early means your child can take confident steps toward their dreams-top colleges, specialized coaching, global experiences, or building new skills for tomorrow’s world.

The Best Time to Start is Now

Planning for your child’s future is a journey shaped by the choices you make today. By starting early, staying consistent, and investing with a clear purpose, you are not just building a corpus, you are creating opportunities, confidence, and freedom for your child’s tomorrow. With the right approach and disciplined investing, you can take small steps toward turning their aspirations into reality.

Be the first believer in your child’s dreams, start Investing today. Visit www.sbimf.com or download our INVESTAP NXT app or visit your nearest SBI Mutual Fund branch. You may also consult your financial advisor for more details.

FAQs:

1. Can I, as a parent, invest in the name of my child from my bank account?

No. Investments can be made only in the name of Minor represented by Guardian (Adult Resident Individuals or Non-Resident Adult Individuals). Payment for investment by means of Cheque, Demand Draft or any other mode shall be accepted from the bank account of the minor or from a joint account of the minor with the guardian only.

2. Can a grandparent or a relative invest in the name of the child?

A grandparent or a relative can only invest in the name of the child only if he/she is the court appointed legal guardian.

3. What happens when the minor turns into a major? Will there be an intimation for the same?

Mutual Fund will send an intimation to Unit holders advising the minor (on attaining majority) to submit an application form along with prescribed documents to change the status of the account from ‘minor’ to ‘major’.

Upon the minor attaining the status of major, the minor in whose name the investment was made, shall be required to provide PAN, KYC details, updated bank account details including cancelled original cheque leaf of the new account. No further transactions shall be allowed till the status of the minor is changed to major

4. Once the minor turns into major, will a joint account be allowed for redemption proceeds?

Once the minor turns into a major, it is expected that he/she should be getting the status updated in the bank account as well. Subsequently the bank account with joint names, 1st being the Major Holder & 2nd being the parent can be registered in the folio. Yes, redemption proceeds can be credited to such accounts.

5. Can I continue to invest in the name of my child after he/she turns 18?

No investments (lumpsum/SIP/ switch in/ STP in etc.) in the scheme would be allowed once the minor attains majority i.e. 18 years of age, till the status is changed to major.

6. After my child turns 18, can I initiate a transaction or the status change from minor to major is required?

All transactions / standing instructions / systematic transactions etc. will be suspended i.e. the Folio will be temporarily frozen for operation by the guardian from the date of beneficiary child completing 18 years of age, till the status of the minor is changed to major. Upon the minor attaining the status of major, the minor in whose name the investment was made, shall be required to provide all the KYC details, updated bank account details including cancelled original cheque leaf of the new bank account.

7. Is there a lock in period in the scheme?

Yes, the scheme has a lock-in for at least 5 years or till the child attains age of majority (whichever is earlier).

8. How many schemes are there in the Solution Oriented – Children’s Fund category?

We have two schemes, i.e. SBI Children’s Fund - Savings Plan which is debt oriented and SBI Children’s Fund - Investment Plan which is equity oriented.

Data as on April 30, 2026

Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.