Change is constant: Disentangling Big Style Shifts

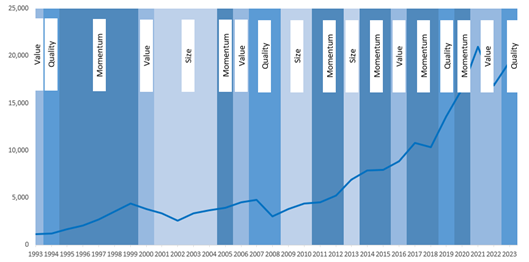

Chart 1 depicts the performance of MSCI USA Index (total

returns, USD) since 1993 till date and we can observe that

valuation, quality, momentum and size have outperformed at

different points in time. MSCI does not consider growth as a

separate factor as it is complementary to the value factor.

MSCI provides an easy and accessible range of well

documented regional factor-based indices dating back to at

least 2002 and is widely used by global investors and ETF

providers.

As observed globally, value as a factor, which dominated the

early decade of the century (with size), made a comeback in

2021-2022, after a decade of dominance of momentum and

growth1. By definition, quality is a defensive factor which

explains why it outperformed during the GFC.

More importantly, factor rotation has increased over the

last decade compared to the end of the 1900s.

Chart 1: Best Performing Factor and the MSCI USA Index

Sources: Factset, MSCI

Sources: Factset, MSCI

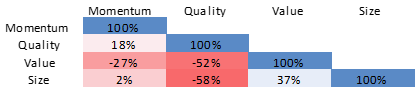

Table 1: Correlation between MSCI US Style Factors

(1993-2023)

There is no unanimity around growth factors. Some simply

considers the factor as an anti-Value factor.

It is interesting, that momentum is hardly correlated to

quality, value and size. One explanation can be that

momentum is simply the consequence of the autocorrelation of

factor returns due to the investor sentiment driven by fear

and greed creating systematic trends over time. If momentum

is simply be an aggregation of autocorrelations of other

factors, it should not be considered as a separate factor.

Not all academics agree but momentum is widely considered as

a factor, especially since the academic works of Jegadeesh

and Titman (1993) and Cahart (1997) were published.

Reassuringly, value and quality factors are anticorrelated.

This is by definition. Quality mimicking portfolios are made

of companies with a strong balance sheet and are profitable.

While value mimicking portfolios are generally composed of

out of flavour or fundamentally distressed stocks.

Similarly, quality and size are anticorrelated. By size, we

mean mid and small cap stocks. One reason can rely on the

fact that mid and small cap companies are generally less

established and less profitable than quality stocks.

It is important to understand the correlation and covariance

between factors because it explains how factors

concomitantly perform and is also a starting point for the

creation of a multi-factor model with uncorrelated

sub-factors.

Identifying market regimes and understanding equity factor

performances provide opportunities to time the market and

equity factors. Lots of academic research has been written

on the topic with varying conclusions. That’s for another

day.

Factor Investing and Factor Regimes in India

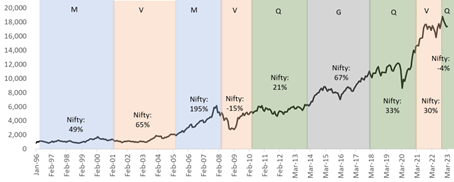

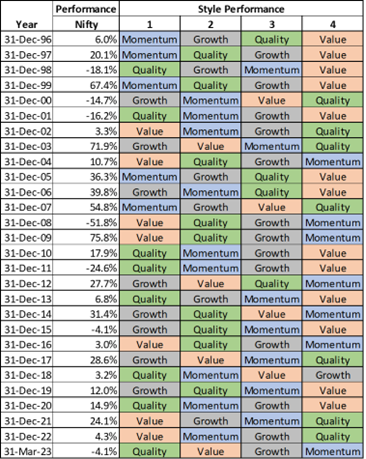

Back home in India, different market regimes have been

favourable for specific styles to outperform. Indian

markets, in the past, have witnessed periods of a particular

style standing out in performance. For our analysis, we have

considered the Nifty 50 as a proxy for Indian markets. Also,

we define growth style with both past earnings parameters &

earnings revision which could be different from academic

research & others such as MSCI. In chart 2, we looked at

Nifty 50 returns across a span of 27 years & the best

performing style in different periods. Duration of these

style regimes have varied with multi-year style periods like

the outperformance of quality from 2009 to 2013. There have

also been shorter style cycles like value performance

between 2007 to 2009. We, also, notice that when momentum or

growth are the top performing style, market return is higher

compared to when quality outperforms.

There are periods of time where factors in India and the

world work alongside and some periods where it is specific

to the market.

Chart 2: Style Performance across Different Regimes

Source: SBI MF Research, Factset M= Momentum, V= Value, Q=

Quality, G= Growth; Returns are long-short returns i.e.,

average of top 2 quintile minus the bottom 2 quintiles.

Quintiles refers to dividing the data set into 5 equal

groups i.e., each being 20% of the data set. The top

quintile is the top 20% of the data set.

Source: SBI MF Research, Factset M= Momentum, V= Value, Q=

Quality, G= Growth; Returns are long-short returns i.e.,

average of top 2 quintile minus the bottom 2 quintiles.

Quintiles refers to dividing the data set into 5 equal

groups i.e., each being 20% of the data set. The top

quintile is the top 20% of the data set.

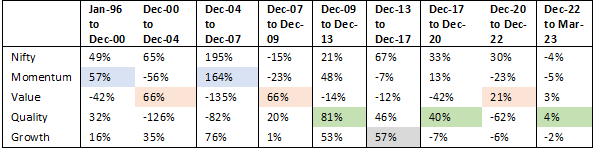

If we look at calendar year performance of different styles

(table 2), quality & growth are the most frequent top

performing styles; however, they outperform during different

market regimes. Growth outperformed when markets gave an

average return of 24%. Quality, however, is the

top-performing style when markets are down with an average

return of -2.5%. Expectedly, quality outperforms when

markets are down.

Table 2: Calendar Year Style Performance

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

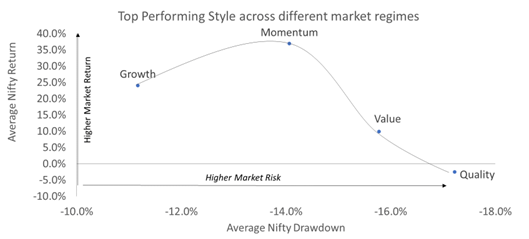

This brings us to the question on whether certain styles

perform in specific market regimes. An insight into style

characteristics helps us to tilt a portfolio based on our

market expectations. In chart 3, we have plotted the average

market return & drawdown when a certain style is the top

performing style in that calendar year. When momentum &

growth are the top-performing styles, average market returns

are higher & drawdown is lower. Value outperforms when

market returns are lower while remaining positive. However,

when value is the top performer, markets have a higher

drawdown. Predictably, quality is the top performing style

when the market average return is negative with the highest

drawdown.

Chart 3: Style Characteristics

Source: SBI MF Research, Factset

Source: SBI MF Research, Factset

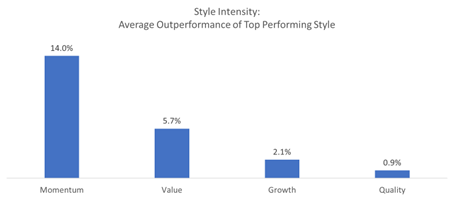

The quantum of outperformance across various styles will

also vary. In chart 4, we measure the style intensity i.e.,

the quantum of outperformance over the market in a year when

that style is the best-performing. Assuming an average

market return in a calendar year is 15%, whenever momentum

is the best performing style, it has the largest

outperformance. On the flipside, in a year when quality tops

the style charts, it has only a marginal outperformance over

markets.

Chart 4: Style Intensity

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

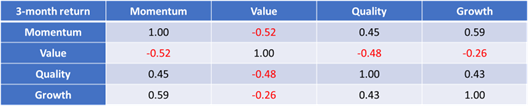

Understanding the correlation of styles helps us to improve

diversification in our portfolios while controlling risk. In

table 3, we look at the 3-month return correlation of

styles. We can see in the table below that value has the

largest negative correlation with momentum & quality. This

suggests that value, typically, will move in an opposite

direction compared to momentum & quality.

Table 3: Style Correlation

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

In chart 5, we compare the 3-year active return of value

over momentum & quality. Periods when the active return is

below 0% are cycles when momentum & quality have

outperformed as styles over value.

Chart 5: 3-year rolling-returns

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the dataset.

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the dataset.

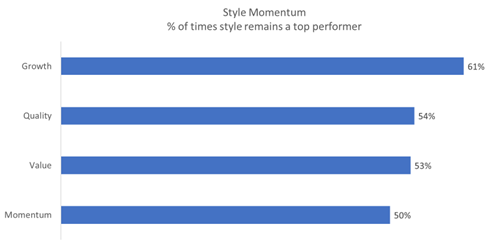

Just like stocks have momentum, styles have the tendency to

persist, in the near term, with their recent performance.

Here, in chart 6, we look at whether a style which is a top

performing style in the previous 2 months retains its

performance in the next month. Growth, as a style, appears

to have the strongest persistence in momentum followed

closely by quality & value.

Chart 6: Style Momentum

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles.6 month return has been considered for the above

calculation. Quintiles refers to dividing the data set

into 5 equal groups i.e., each being 20% of the data set.

The top quintile is the top 20% of the data set.

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles.6 month return has been considered for the above

calculation. Quintiles refers to dividing the data set

into 5 equal groups i.e., each being 20% of the data set.

The top quintile is the top 20% of the data set.

Another interesting question could be whether style

performance in US markets are lead indicators for style

performance in Indian markets. While the correlation

coefficient doesn’t seem to be significantly high, 3-month

quality performance in the US has a negative correlation

with forward 6-month India momentum & growth style returns.

Table 4: Correlation with US Style Factors

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

Source: SBI MF Research, Factset Returns are long-short

returns i.e., average of top 2 quintile minus the bottom 2

quintiles. Quintiles refers to dividing the data set into

5 equal groups i.e., each being 20% of the data set. The

top quintile is the top 20% of the data set.

Appendix:

Momentum: In the momentum factor, stocks are ranked based on

their near to medium term performance. Stocks that have

performed in the near term are ranked higher than laggards.

We look at parameters such as 6- & 12-month price

performance, 1 month price reversion, nearness to 52-week

high, etc.

Value: In the value factor, stocks are ranked based on

various valuation ratios; inexpensive stocks relative to

their fundamentals are ranked higher. In the Value factor,

we look at parameters such as price to earnings, price to

book value, enterprise value to sales, dividend yield etc.

Quality: In the quality factor, stocks are ranked based on

various earnings & balance sheet parameters such that high

quality stocks with stable earnings & robust business models

are ranked higher. This is a defensive factor; we look at

parameters such as return on equity, leverage, earnings risk

etc.

Growth: In the growth factor, stocks are ranked based on

various historical earnings, expected earnings & consensus

ratings such that high growth stocks with higher

expectations are ranked higher. In the growth factor, we

look at parameters such as trailing earnings growth,

consensus earnings revision, consensus earnings upgrades to

downgrades, etc.

This presentation is for information purposes only and is

not an offer to sell or a solicitation to buy any mutual

fund units/securities. The views expressed herein are based

on the basis of internal data, publicly available

information & other sources believed to be reliable. Any

calculations made are approximations meant as guidelines

only, which need to be confirmed before relying on them.

These views alone are not sufficient and should not be used

for the development or implementation of an investment

strategy. It should not be construed as investment advice to

any party. All opinions and estimates included here

constitute our view as of this date and are subject to

change without notice. Neither SBI Funds Management Limited,

SBI Mutual Fund nor any person connected with it, accepts

any liability arising from the use of this information. The

recipient of this material should rely on their

investigations and take their own professional advice.

)

)